The Reserve Bank of India (RBI) has kept the benchmark repo rate unchanged at 6.5% for the eleventh time. This decision reflects the RBI’s careful approach to managing inflation and monetary policy. While some sectors, including real estate, were expecting a rate cut to stimulate demand, the move aims to ensure market stability. It also provides homebuyers with clarity on interest rates as they deal with rising property prices and evaluate the impact on home loan EMIs.

Stability for Homebuyers

For homebuyers with existing home loans, the RBI's decision to keep the repo rate steady means that their EMIs will remain unchanged. In a market where property prices are continuing to climb, this stability in EMIs offers some relief. Homebuyers do not have to worry about sudden interest rate hikes, which allows them to plan their finances more effectively.

However, while the repo rate stability is beneficial in terms of EMIs, it does not address the larger issue of rising property prices. According to ANAROCK Research, property prices in India’s top seven cities have risen by 23% between Q3 2023 and Q3 2024. This surge, combined with the unchanged interest rate, has led to a decline in housing sales, with transactions dropping by about 11% year-on-year in Q3 2024. The combination of high property prices and stable interest rates has led to reduced demand in some market segments.

As per Mr. G Hari Babu National President of NAREDCO, “The Reserve Bank of India’s decision to maintain the repo rate at 6.5% and reduce the cash reserve ratio (CRR) by 50 basis points to 4% is a balanced approach to sustaining economic stability while fostering liquidity. This move aligns with the real estate sector’s ongoing need for growth support amid evolving market dynamics.

The unchanged repo rate ensures continued affordability for homebuyers and stability in lending rates, both critical factors in sustaining the demand momentum witnessed in residential and commercial real estate. The reduction in CRR is a welcome step, as it releases additional liquidity into the banking system, providing financial institutions with greater flexibility to offer loans at competitive rates."

He further added, "Buyer sentiment in the real estate sector remains positive, and real estate has received the highest investment of 17% in Alternative Investment Funds during the first half of 2024-25. This move by the RBI will further boost the real estate sector. However, we hope that the RBI will consider reducing repo rates in its next decision to give a greater impetus to affordable housing

For the real estate sector, liquidity is pivotal in driving construction activity and meeting delivery timelines, especially for affordable housing projects that cater to a significant segment of aspiring homeowners. The neutral stance reflects a careful consideration of inflationary pressures and economic growth, which reassures the industry of a stable monetary policy environment. This policy announcement underscores the RBI’s commitment to creating an enabling ecosystem for businesses and consumers alike. The real estate industry remains optimistic about its role in contributing to India’s economic growth trajectory under such supportive measures.”

Impact on the Real Estate Market

The RBI's decision to maintain interest rates at 6.5% has implications for the real estate market. Developers, who were hoping for a rate cut to spur demand, are feeling the effects of slow sales in the face of rising property prices. In addition, the RBI recently reduced the Cash Reserve Ratio (CRR) from 4.5% to 4%, a move aimed at increasing liquidity in the banking system. This change will release ₹1.16 lakh crore into the system, which is expected to help increase the lending capacity of banks and eventually make loans more accessible and potentially more affordable in the future. However, the full impact of this change may take time to unfold.

Many real estate developers remain hopeful that the RBI will lower the repo rate in the coming months. Such a move could help ease the financial burden on homebuyers and provide developers with more favorable borrowing terms for new projects.

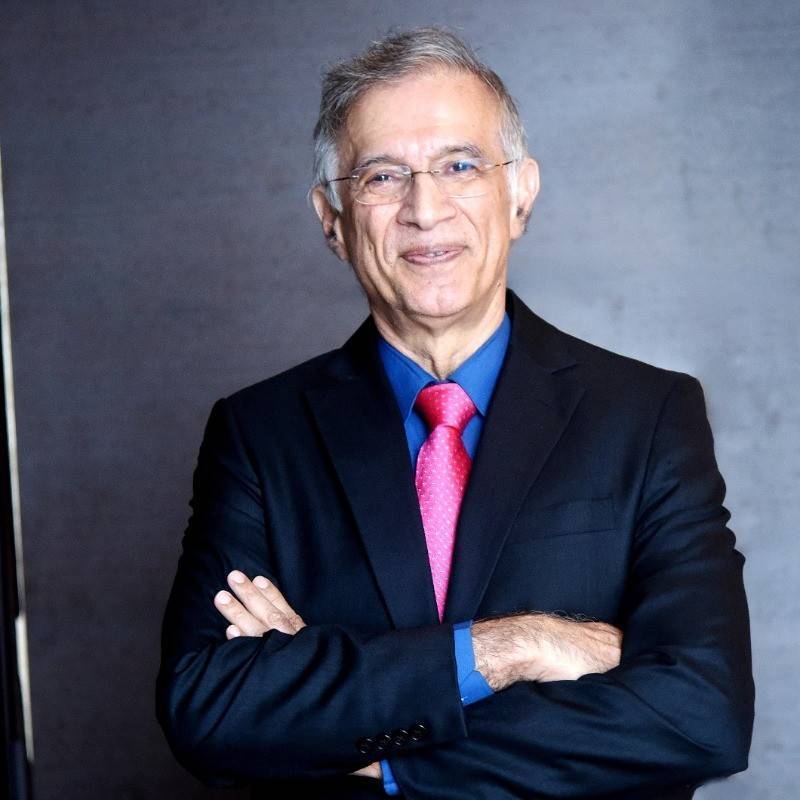

As per, Piyush Bothra, Co-Founder & CFO, Square Yards, “The RBI's decision to keep the repo rate unchanged is slightly disappointing, as the general expectation was for a rate cut of at least 25 basis points. However, the decision to reduce the Credit Reserve Ratio (CRR)) by 50 basis points is expected to help increase liquidity in the banking system and boost overall credit disbursements. The real estate sector continues to be buoyed by significant pent-up demand and improved affordability. We do not anticipate any negative impact from the unchanged rates on demand as we enter the final quarter, which is traditionally the strongest quarter of the financial year.”

The Call for a Rate Cut

Real estate experts have been pushing for a rate cut, particularly for the affordable housing sector, which has seen slower sales due to the higher cost of borrowing. Shishir Baijal, Chairman of Knight Frank India, has pointed out the challenges in the affordable housing segment, where demand has fallen because higher interest rates have made loans less accessible to potential buyers.

A rate cut could help increase demand in the mid-range and affordable housing sectors. Lower interest rates would make home loans more accessible, encouraging more people to purchase homes, even as property prices continue to rise. Increased demand could help stimulate the housing market and positively affect the broader economy by improving consumer sentiment.

Looking Ahead

As we move forward, the outlook for the real estate sector remains cautious but hopeful. While demand may pick up during the festive season, industry experts are focusing on the RBI’s next policy review in February 2025. If the central bank decides to reduce rates, it could significantly improve housing affordability and stimulate demand in the housing market.

In the short term, however, the current rate decision may not lead to significant improvement in the sector. Developers are likely to continue facing challenges, as borrowing costs remain high and sales continue to slow. Nonetheless, there is an expectation that any future rate cuts will offer relief to homebuyers, making housing more affordable and potentially driving growth in the sector.

For now, the RBI’s decision to hold the repo rate steady at 6.5% provides stability, which helps with planning for both homebuyers and developers. While this decision may not be a complete solution to the challenges facing the real estate market, it offers some predictability. The hope is that, with future rate cuts and other policy measures, the housing market will become more vibrant and accessible in the months ahead.