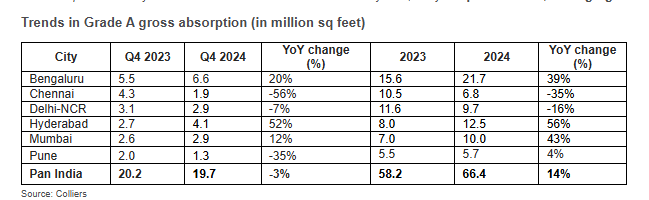

As per Colliers Report, the office market in 2024 has achieved significant growth, with leasing activity across the top six cities reaching 66.4 million sq feet. This corresponds to a strong 14% growth year-on-year in leasing activity. Bengaluru drove Grade A office space demand, with highest-ever leasing volume of 21.7 million square feet, marking an impressive 40% YoY increase. Demand scale-up was also evident in Hyderabad and Mumbai. With 12.5 and 10.0 million sq feet of leasing activity respectively, both cities witnessed double-digit annual office space demand for the first time in 2024. Meanwhile, Delhi-NCR too witnessed healthy space uptake and Grade A demand almost touched 10 million sq feet mark in 2024. This remarkable activity across major office markets has propelled office leasing to new heights and established new demand benchmarks at the India level.

A strong final quarter propels record-breaking leasing activity in key cities

2024 has exhibited consistent demand growth throughout the year, with leasing activity in each quarter surpassing the previous quarter. Q4 2024 saw the highest leasing during the year, at 19.7 million sq feet, a 14% increase over the previous quarter. Hyderabad and Bengaluru led leasing activity during Q4 2024, collectively contributing to 54% of India leasing during the quarter. Amongst the top six cities, while quarterly leasing was highest in Bengaluru at 6.6 million sq feet, QoQ demand growth was highest in Mumbai & Hyderabad at 71% and 41% respectively.

“After witnessing higher space uptake in successive quarters, Grade A office space demand in India has broken all past records and registered 66.4 million sq feet of activity in 2024. Three out of the six major cities witnessed more than 10 million sq feet of annual leasing. Bengaluru especially witnessed remarkably strong demand of close to 22 million sq feet and accounted for one-third of the total space uptake in 2024. New supply during the year also remained above the 50 million sq feet mark and kept vacancy levels rangebound. 2025 demand can potentially stabilize at elevated levels and annual space uptake exceeding 60 million sq feet is likely to be the new norm over the next few years,” says Arpit Mehrotra, Managing Director, Office services, India, Colliers.

Gross absorption: does not include lease renewals, pre-commitments and deals where only a letter of Intent has been signed.

Top 6 cities include Bengaluru, Chennai, Delhi-NCR, Hyderabad, Mumbai, and Pune

Gross supply: does not include lease renewals, pre-commitments and deals where only a letter of Intent has been signed.

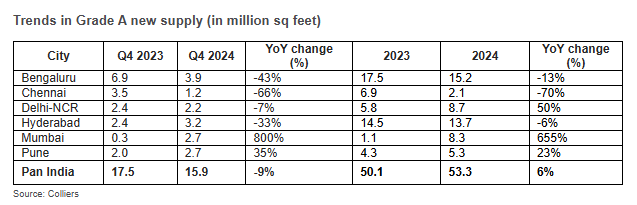

Top 6 cities include Bengaluru, Chennai, Delhi-NCR, Hyderabad, Mumbai, and Pune

Flex space leasing touches new quarterly and annual high

At 4.7 million sq feet, flex spaces saw their highest ever quarterly leasing. Interestingly, of all the demand sectors, flex space demand was the highest and accounted for 24% of the Grade A space uptake in Q4 2024. Strong flex activity throughout the year has propelled flex space demand to a record annual absorption of 12.5 million sq feet, a 45% YoY growth. While technology sector continued to drive annual office space demand with almost one-fourth share in overall leasing, flex spaces accounted for almost one-fifth of the Grade A space uptake in 2024. BFSI and engineering & manufacturing sectors too demonstrated healthy leasing activity, both crossing the 10 million sq feet leasing in 2024. Notably, large-sized deals (≥100,000 sq feet) continued to drive leasing activity and contributed to 54% of total demand in 2024. Large-sized deals were particularly preferred by occupiers from the technology sector and flex spaces as well.

Data pertains to Grade A buildings only

“Annual flex space leasing has comfortably surpassed 10 million sq feet mark for the first time, eventually registering Grade A space uptake of 12.5 million sq feet in 2024, a remarkable 45% year-on-year increase. Delhi-NCR, followed by Bengaluru, together accounted for over half of the total flex space leasing during the year. Flex space activity has grown significantly in 2024. Flex operators accounted for almost 20% of the India office space demand in 2024, up from 5-15% share in each of the years starting 2020. The occupier preference for managed office spaces augurs well for leading operators, who are likely to increasingly foray into Tier-II/III cities throughout 2025 and expedite their fund-raising plans through primary markets as well,” said Vimal Nadar, Senior Director and Head of Research, Colliers India.

New supply follows demand in most cities, vacancy levels remain rangebound

On the supply side, Q4 2024 witnessed 15.9 million sq feet of new completions, pushing the total to 53.3 million sq feet for the year, a 6% growth compared to 2023. Bengaluru and Hyderabad were the major contributors and cumulatively accounted for 54% of the new supply during 2024. With demand exceeding new supply across most cities, overall India vacancy levels declined by 80 basis points on an annual basis. Rentals meanwhile increased by 5%, compared to 2023.