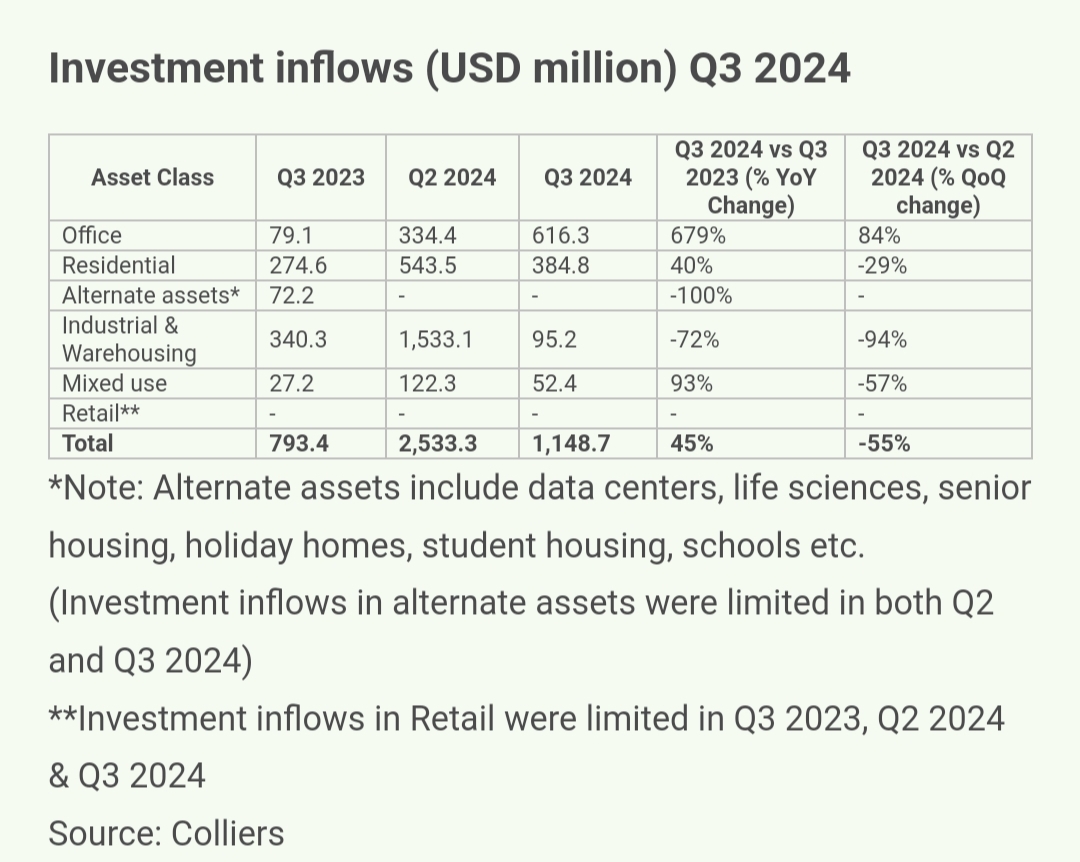

Sustained confidence in the Indian economy continued to drive institutional investments into the real estate sector, reaching USD 4.7 billion during the first three quarters of 2024, almost at par with the corresponding period in 2023. Following significant inflows in the first two quarters, Q3 2024 registered a healthy investment inflow of about USD 1.1 billion, reflecting a 45% YoY growth. Office segment accounted for 54% of the total investments during the quarter, followed by residential, with a 33% share. Residential inflows during Q3 2024 were particularly driven by domestic capital. Overall domestic investments remained robust at USD 0.5 billion, driving 44% of the total inflows during the quarter.

“Institutional flows in Indian realty remain consistent, indicating sustained investor confidence. The investors are well diversified between global and domestic capital. While office assets remain a key focus, industrial & warehousing and residential segments are gaining significant momentum. The newer emerging themes like fractional ownership in office & warehousing, residential platforms with developers, flexible credit, and hospitality are driving opportunities for investors. Of the total USD 4.7 billion institutional inflows during the first nine months of 2024 (Jan-Sept), over 60% were directed towards industrial & warehousing and residential assets. With continued momentum, 2024 is expected to end on a higher note, likely surpassing 2023 volumes,” said Piyush Gupta, Managing Director, Capital Markets & Investment Services at Colliers India.

In addition to continued traction in domestic capital, foreign investors also maintained a sizable and a healthy appetite for Indian real estate. At USD 0.6 billion inflows in Q3 2024, foreign investments have more than doubled compared to the investments witnessed in Q3 2023.

Quarterly investments in Office segment surged by 6.8X times over Q3 2023

After witnessing subdued activity in the previous quarter, investments in the office segment doubled on a QoQ basis, at USD 0.6 billion inflows. At the same time, investments also rose by 6.8X times as compared to the same period last year. Foreign investments accounted for 88% of the total inflows into the segment during Q3 2024.

Going forward, robust demand and supply momentum in Grade A office spaces across the top markets will keep the investor confidence buoyant. Apart from office assets, residential assets too witnessed notable inflows during the quarter at USD 0.4 billion, witnessing a substantial surge of 40% on a YoY basis.

"Private equity investments in the residential segment are on the rise, fuelled by home-ownership trends and growing interest from domestic as well as foreign institutional investors. In the first nine months of 2024, investments in the segment crossed USD 1 billion, marking a significant 46% year-on-year increase. Q3 2024 alone saw USD 0.4 billion in residential investments, accounting for one-third of the total investments in the quarter. Most of these investments were directed towards developmental assets, as institutional investors continue to partner with reputed developers in marquee residential projects. With a conducive domestic environment, ongoing festive season and a much-anticipated reduction in interest rates, investor confidence in India's residential real estate market is poised to remain intact," said Vimal Nadar, Senior Director and Head of Research, Colliers India.

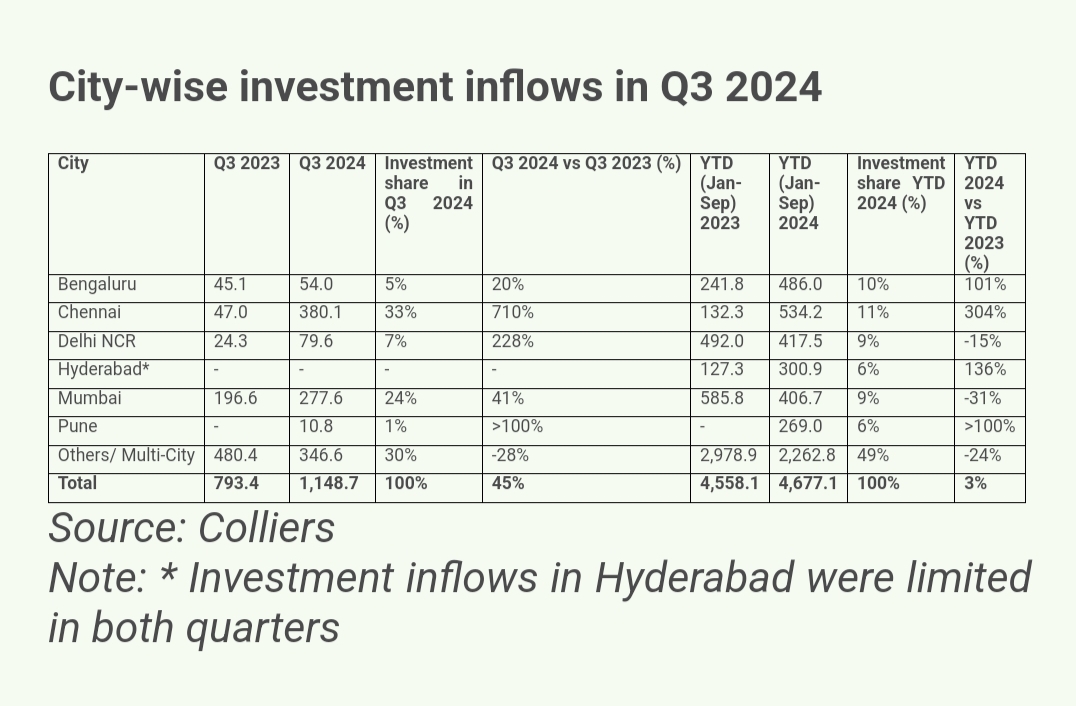

Chennai & Mumbai together drove about 57% of the quarterly inflows

Chennai and Mumbai together accounted for about 57% of the total inflows during Q3 2024 backed by key acquisitions in the office segment. Almost 70% of the inflows in Chennai during the quarter were driven by foreign investments. Mumbai and Delhi NCR cumulatively witnessed about 44% of the total quarterly investments in the residential segment. Furthermore, multi-city investments corresponded to 30% of the overall inflows during Q3 2024 and were predominantly directed towards office and residential asset classes.

Conclusion

The Indian real estate sector continues to witness strong institutional investment inflows, with Q3 2024 recording a significant 45% year-on-year growth, reaching USD 1.1 billion. The office and residential segments remain key drivers of this momentum, supported by both domestic and foreign capital. Cities like Chennai and Mumbai played a pivotal role, attracting the majority of the investments. With investor confidence buoyed by robust demand, supply in Grade A office spaces, and growing interest in residential projects, the realty sector is poised for further growth. As emerging investment themes gain traction, the overall outlook for 4 suggests a promising finish, likely surpassing the previous year's performance.

.png)