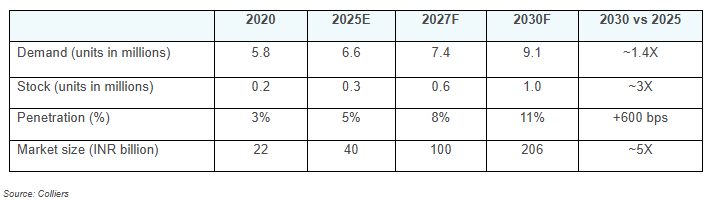

India’s co-living market is on an upward growth trajectory, with demand rebounding strongly in recent years and operators gearing up for expansion across Tier I cities and select Tier II cities. Currently estimated at around 0.3 million beds in the organized market, the inventory is projected to grow more than threefold and reach close to a whopping 1 million beds by 2030. The resurgence of the sector is being fueled by rapid urbanization and migration to cities, especially amongst students and young professionals who continue to seek flexible, relatively affordable, community-driven, and hassle-free housing options.

Following a temporary lull during the pandemic, the demand for co-living is regaining momentum, driven by the inherent strengths of the sector. Evolving demographic patterns, education & employment-driven urban migration, rising disposable incomes, and a growing preference for fully managed rental accommodations are all contributing to a sustained rise in demand for organized co-living spaces. Of the estimated 50 million migrant population in urban India aged between 20 & 34 years in 2025, the demand base for organized co-living sector in terms of beds is currently estimated at 6.6 million.

Co-living inventory, meanwhile, stands at around 0.3 million beds only, translating into a penetration rate of about 5%. Given the intrinsic nature of demand, leading operators are in an expansionary mode. As the co-living inventory is set to reach close to 1 million beds by 2030, penetration rates can significantly improve from 5% to over 10% by the end of the decade.

“India’s co-living sector is entering a new phase of growth, underpinned by strong demographic fundamentals and a growing preference for flexible, community-centric living. With rapid urbanization and a high proportion of migrant population, including students & young working professionals, the demand for organized rental housing, especially co-living, is likely to witness strong growth. Significant upside potential is anticipated to provide thrust to investor participation and operator expansion in the co-living sector. Resultantly, we expect market penetration to double from ~5% currently to over 10% by 2030. In fact, the coming years will be crucial in shaping a more structured, scalable, and investment-ready co-living ecosystem in India”, said Badal Yagnik, Chief Executive Officer, Colliers India.

Trends in India’s co-living market

Note: E is estimated and F stands for forecasted numbers by the end of the year

Demand is estimated by projecting the urban migrant population aged 20–34, primarily relocating to urban areas for employment and studies. The demand projection assumes that a meaningful share of this demographic prefers co-living over traditional rental housing due to convenience, affordability, and lifestyle alignment.

Demand estimations take into account urban population in the 20–34 yrs age group and employment opportunity & higher education-driven urban migration. Demand estimates also factor in a proportion/representative profile within the urban migrant population having economic ability and preference for co-living accommodation over traditional rental housing due to convenience, lifestyle alignment etc.

The co-living market size is estimated on the basis of current/projected stock, adjusted for occupancy levels. Average monthly rentals provide an indication on annual revenues/market size of the sector.

Co-living penetration represents the ratio of organized inventory (in terms of beds) and the demand for co-living accommodation within the target population, primarily urban migrants, including students and young working professionals

“Robust growth coupled with significant untapped potential presents the co-living sector as an increasingly attractive asset class within real estate contours in India. While leading operators continue to consolidate their presence in the Tier I cities, we are already witnessing steady expansion into select Tier II markets such as Indore, Coimbatore, Chandigarh, Jaipur, Visakhapatnam, Dehradun etc. The co-living market, estimated at around INR 40 billion in 2025, has the potential to grow over five times and reach close to INR 200 billion by 2030. As institutional investors get adept with risk-return dynamics of managed rental accommodation, the co-living sector is well-positioned to enter its next phase of growth marked by broader geographical reach and value-additions in market offerings.”, said Vimal Nadar, National Director & Head of Research, Colliers India.

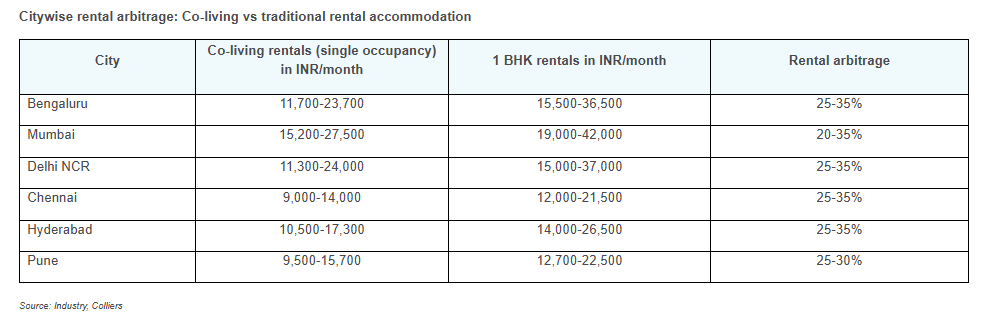

Co-living offers 20–35% rental arbitrage as compared to traditional rental accommodations

Typical co-living facilities provide fully furnished, ready-to-move-in spaces at rentals inclusive of utilities, maintenance, and amenities like Wi-Fi, housekeeping, and community events. This ensures convenience and cost-effectiveness for the target segment - young professionals and students. Co-living facilities also foster a sense of community through shared spaces and curated social interactions, reducing the feeling of isolation in urban environments. Additionally, flexible stay durations and minimal upfront costs make co-living a more amenable and hassle-free alternative to traditional rental accommodation.

Overall, co-living spaces offer a more affordable alternative across major Indian cities. As of April 2025, a comparison of rents between single-occupancy co-living facilities and traditional 1 BHK units indicates a rental arbitrage of up to 35%.

Note: Monthly rentals of traditional 1 BHK apartment units include utility expenses and maintenance charges

Co-living rents are typically inclusive of shared amenity access, utility, housekeeping, and basic furnishing charges etc.

Rental arbitrage is a comparison of typical rentals for single occupancy in co-living properties and 1BHK rentals in the same locality.

Capital deployment in the co-living sector bolstered by relatively higher returns

Leading co-living operators in India are actively raising capital to scale up their operations, particularly in light of the growing demand from students and young professionals. Leading operators have collectively raised capital to the tune of USD 1 billion since inception (2015 onwards), underscoring investor confidence and long-term growth potential. Institutional investors too are increasingly viewing co-living as an attractive asset class, with returns closer to 10%, significantly higher than the 2-5% yield of traditional residential assets. In fact, steady rental income, asset-light model, and alignment with the lifestyle preferences of younger generations support diversification of capital deployment by institutional investors. As the co-living gets formalized to a greater degree in India, improving operator efficiencies and expansion are likely to accelerate the sector’s transition into a relatively matured real estate asset class in the upcoming years.

Lease-based model most preferred by top co-living operators

India’s co-living landscape is evolving rapidly, with distinct business models aimed at balancing scalability, capital efficiency, and service delivery. Broadly, the sector operates through three primary models: lease, management/revenue-sharing, and franchise:

- Lease model - Majority of the active operators prefer an asset-light approach and lease residential units or entire buildings from property owners and then rent them out to end-users. Typical lease agreements between operators and property owners range between 3 to 9 years. The lease model minimizes upfront capital expenditure and allows for faster expansion.

- Management/revenue sharing model - Under this model, the co-living operator manages the property and takes a share of monthly or annual revenue. This approach aligns with the interests of both property owners and operators, as both parties tend to have a proportionate exposure to occupancy levels.

- Franchise model - In the franchise model, operators allow property owners to use their brand and access enterprise resources like marketing and technology in lieu of franchisee fees. The franchise model enables rapid expansion into Tier-2 and Tier-3 cities through local partners.

Regardless of the model, co-living operators aim to offer serviced living experience, typically via tech-enabled platforms that cover housekeeping, maintenance, laundry, and more. Typically, most services are bundled in a composite rent for the end-user, with food being billed separately.

Additionally, select co-living operators have ventured into Purpose-Built Student Accommodation (PBSA) by partnering with leading educational institutions. Although PBSA facilities, owned and managed directly by the operator, allow greater control over the asset, they involve substantial capital investment.

Demand-supply gap in student housing presents immense opportunities for investors and operators within the co-living sector

While co-living facilities are targeted at both students and migrant working professionals alike, student housing is more nuanced and is an important sub-segment within the co-living sector. Currently, approximately 11% of India’s population is in the 18-23 years age group. Although, enrollment in higher education remains low compared to developed countries and is indicated by a Gross Enrollment Ratio (GER) of 28.4% at the national level (2021-2022), enrollments in absolute terms remain huge. The number of students enrolled in higher education courses, including graduate and postgraduate programs, rose from 30.2 million in FY 2012-13 to 43.3 million in FY 2021-22, witnessing a CAGR of 3.7%.

A significant proportion of higher education students enrolled in India are out-station students who require accommodation facilities near their institutions. As per All India Survey on Higher Education (AISHE), during FY2021-22, accommodation facilities provided by colleges & universities could cater to approximately 4 million students, merely 35-40% of the demand and resulting in a significant demand-supply mismatch. As of 2025, the demand for student-living accommodation is estimated to be around 12 million. The acute demand and supply gap necessitates the need for quality, affordable accommodation, especially as more students migrate to cities for higher education. It also presents immense opportunities for student housing-focused operators to foray into the market with professionally managed, student-centric housing solutions that can alleviate supply-side constraints and support the evolving needs of India’s student population.

.png)