India’s Housing Market in 2025: Key Highlights (PropTiger Report)

- Residential sales moderated in 2025, declining 12% YoY to 3.86 lakh units, marking the lowest annual sales since 2022, reflecting demand recalibration rather than contraction.

- Q4 2025 recorded the weakest quarterly sales since Q2 2023, with volumes down 10% YoY, indicating cautious buyer behaviour amid macro uncertainty.

- New housing supply fell 6% YoY, touching its lowest level since 2021, as developers adopted disciplined and calibrated launch strategies.

- City-level performance diverged sharply, with Chennai and Hyderabad emerging as consistent outperformers, while Delhi NCR remained under prolonged consolidation.

- Residential prices stayed firm despite softer volumes, supported by limited ready inventory, rising construction costs, and strong pricing discipline by developers.

India's residential real estate market gradually returned to normal during 2025 with housing demand weakening from the peak levels of the previous two years but still remaining quite resilient at the core. The housing market report for the whole year 2025 titled Real Insight Residential CY 2025 and published by PropTiger.com reveals that such a moderation is a healthy rebalancing of the situation rather than an indication of a permanent lull. Rising base effects, buyers' selectiveness and a gradual change in demand pattern towards end user, driven consumption were among the major factors that caused the market to stabilize whereas the long term drivers such as urbanisation, income growth and infrastructure spending still provide support.

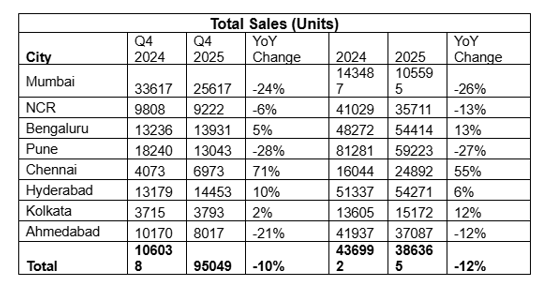

Residential sales across the top eight cities in India were down by 12% year on year to 3, 86, 365 units in 2025 as compared to 4, 36, 992 units in 2024. This was the lowest level of annual sales since 2022, thus, the post-pandemic rally had come to an end. Nevertheless, the market experts had already factored in the extent of decline to a large degree since it had been pumped up by record, breaking sales over the past years. Most importantly, despite the fall, the volume of sales was still significantly higher than the pre-pandemic average, thus, the sector remains very deep and buyers are still confident.

Quarterly change during the year further reveal this gradual moderation. Residential sales in Q4 2025 were 10% lower than in the same quarter of the previous year, and there was a slight drop of 0.5% in sales on a quarter, to, quarter basis down to 95, 049 units. This number represents the lowest quarterly sales since Q2 2023, when sales were at 80, 250 units. The final quarter's lackluster performance was partly the result of buyers making more cautious decisions in the face of price firmness and supply being selectively added, especially for mid, to, premium home segments.

2025, in general, saw quarterly sales gradually decreasing from 98, 095 units in Q1 to 95, 049 units in Q4, which is indicative of demand being postponed rather than a fall in demand. It seems to be that buyers took a more thoughtful approach and focused on project quality, location and credibility of the developer.

The trend points towards a more mature housing market where growth is less reliant on speculation and more on being sustainable, thus, providing a stable base for a balanced expansion over the next few years.

Mr. Onkar Shetye, Executive Director of Aurum PropTech said, “2025 was not a year of demand destruction, but one of recalibration. Buyers remained active but more deliberate, while developers responded with disciplined supply management. This prevented inventory stress and helped prices remain resilient despite softer volumes.”

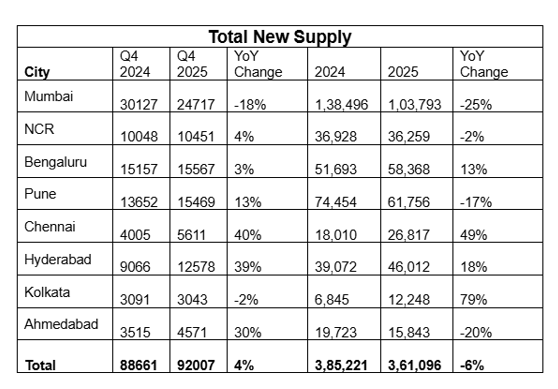

The slowdown was most pronounced in Q2 2025, which emerged as the weakest quarter in terms of new supply due to seasonal factors and heightened buyer caution. However, deferred demand was absorbed steadily in the second half of the year, particularly in southern markets.

City-level divergence widened throughout the year.

Hyderabad and Chennai emerged as consistent outperformers, recording sustained quarterly and year-on-year growth, while Mumbai and Bengaluru displayed volatility but closed the year on a firmer footing. Delhi NCR remained the only major market to record year-on-year sales declines across all four quarters, reflecting prolonged consolidation.

The total new supply across the eight cities fell 6% to 3,61,096 units in 2025 as against 3,85,221 units in 2024. This is the lowest annual supply since 2021.

In the October-December (Q4) 2025, supply rose 4% YoY and 0.2% QoQ to 92007 units.

Despite moderated sales, residential prices continued to rise across key markets, supported by limited ready inventory, elevated construction costs, and calibrated new supply. Developers largely avoided aggressive discounting, reinforcing pricing discipline.

“The housing market is transitioning into a more mature, execution-led phase,” added Mr. Onkar Shetye. Growth in 2026 is likely to be driven by affordability, infrastructure-led micro-markets, and city-specific fundamentals rather than broad-based acceleration.”

Going forward, the residential real estate market in India is predicted to move along a steady, quality, led growth trajectory rather than a fast expansion one.

Demand shifting towards end, users, developers will probably stay disciplined regarding new launches by focusing on execution, project credibility, and location, specific offerings. Infrastructure development, better affordability in few micro, markets, and stable macroeconomic fundamentals will support buyer sentiment, whereas calibrated supply will act as a check on inventory stress. Hence, 2026 may witness balanced growth influenced by city, specific dynamics, sustainable pricing, and a maturing market that favors long, term value over short, term volume.