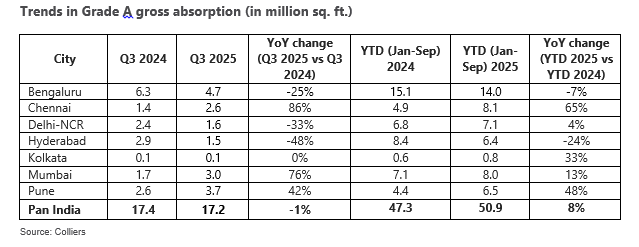

According to Colliers report, leasing activity across India’s top seven office markets has continued to remain upbeat in the first three quarters of 2025. Space uptake for the year has reached 50.9 million sq. ft., marking an 8% YoY growth. However, on a quarterly basis, it dipped marginally to 17.2 million sq. ft. in Q3 2025.

While Bengaluru continued to drive overall transaction volumes in the third quarter, Pune, Mumbai and Chennai, particularly witnessed high demand traction. The three cities cumulatively accounted for more than half of the quarterly Grade A office space uptake. Notably, each of the three cities saw a YoY demand growth of at least 40% in Q3 2025.

In terms of 9-month space uptake, Bengaluru retained its dominance with 14 million sq. ft. of leasing and 27% share in the overall India office space demand. Interestingly, Grade A space uptake has been more evenly balanced in Chennai, Delhi NCR, Hyderabad, Mumbai & Pune. Each of these five cities have already witnessed leasing activity to the tune of 6–8 million square feet in 2025, underscoring the momentum across most major cities of the country.

“India’s office market continues to demonstrate resilience, crossing the 50 million square feet benchmark in the first nine months of the year, despite ongoing external volatilities and trade frictions. This steady momentum has been fueled by a surge in space uptake by GCCs and continued traction in leasing activity from domestic firms. GCCs have already leased close to 20 million sq. ft. in 2025 across the top seven cities, contributing around 40% of the overall office space demand. Going forward, although occupiers are likely to carefully evaluate evolving scenarios, global technology firms will continue to bolster Grade A space uptake and play a pivotal role in driving the office space demand close to 70 million sq. ft. by the end of the year,” said Arpit Mehrotra, Managing Director, Office services, India, Colliers.

Gross absorption does not include lease renewals, pre-commitments and deals where only a letter of Intent has been signed.

Top 7 cities include Bengaluru, Chennai, Delhi-NCR, Hyderabad, Kolkata, Mumbai, and Pune

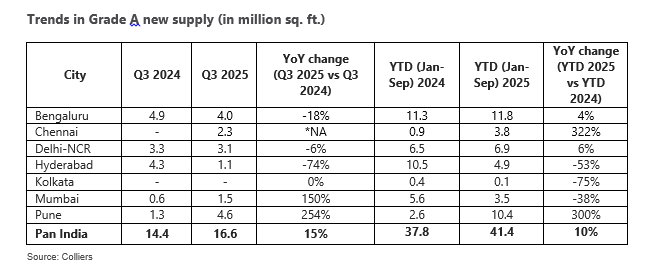

Bengaluru & Pune together drive more than half of the new supply in 2025

New supply across the top seven office markets remained robust in Q3 2025, with 16.6 million square feet of completions, marking a 15% YoY increase. Pune led the momentum with a nearly 4X surge in quarterly completions at 4.6 million square feet, followed by Bengaluru and Delhi-NCR. New supply reached 41.4 million square feet in the first 9 months of 2025, with Bengaluru and Pune together contributing 54% of the new supply. Meanwhile, new completions have been relatively lower in Hyderabad, Mumbai and Kolkata as compared to the corresponding period in 2024.

Top 7 cities include Bengaluru, Chennai, Delhi-NCR, Hyderabad, Kolkata, Mumbai, and Pune

*NA-Not applicable as supply additions were limited in Chennai in Q3 2024; Supply additions were limited in Kolkata during Q3 2024 and Q3 2025

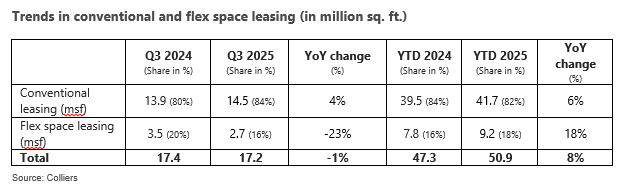

Technology sector occupiers drive 36% of conventional space uptake; BFSI and flex space activity remain strong in 2025

Data pertains to top 7 cities - Bengaluru, Chennai, Delhi-NCR, Hyderabad, Kolkata, Mumbai, and Pune

Conventional leasing in the first nine months of 2025 stood at 41.7 million sq. ft., led primarily by the Technology and BFSI sectors. Technology firms alone leased over 15 million sq. ft., a robust 24% YoY growth, largely driven by the expansion of Global Capability Centers (GCCs). This underscores the technology sector’s pivotal role in shaping the scale and quality of demand. During this 9-month period, flex space leasing reached close to the all-time high, at 9.2 million square feet, reflecting the increasing trend of dynamic real estate requirements.

On a quarterly basis, conventional spaces accounted for 84% of the 17.2 million square feet of Grade A office space uptake in Q3 2025. Flex activity, meanwhile, also remained strong in the third quarter with 2.7 million square feet of space uptake.

“Office space demand in Q3 2025 was driven by technology sector occupiers and BFSI firms, which cumulatively drove nearly 60% of the conventional space uptake. Bengaluru continued to be the epicentre of tech leasing, while Pune emerged as the key driver of BFSI demand, accounting for over 40% of the finance-sector demand in the third quarter. In terms of flex space activity, Bengaluru, along with Pune and Chennai, collectively accounted for nearly two-thirds of the flex space uptake in Q3 2025. Overall, the preference for agile workplace strategies and flex space adoption continues to be on the upswing across India and can potentially account for one-fifth of the overall demand in 2025,” said Vimal Nadar, National Director and Head of Research, Colliers India.

Vacancy levels remain rangebound; while rentals continue to rise across most cities

Despite office space demand exceeding new supply across most cities in Q3 2025, vacancy levels remained rangebound on account of relocations and churns. While vacancy levels at the India level remained steady at 16.4%, Pune and Delhi-NCR witnessed a rise in vacancy levels by over 100 basis points on a quarterly basis, owing to significant new completions. Meanwhile, average rentals continued their upward trajectory across major markets, supported by robust demand-supply dynamics. However, the India office market with its wide rental spectrum across cities and micro markets, continues to present an attractive proposition for global players to consolidate their operations in the country.

.png)