According to Vestian Report, the top ten micro-markets by absorption continued to dominate in Q3 2025, accounting for 70% of the pan-India absorption. However, its share has gradually dropped from 82% in Q3 2024 and 80% in Q2 2025.

In terms of value, the top 10 micro-markets reported an absorption of 13.9 Mn sq ft in Q3 2025, registering a decline of 10% over the year and 8% compared to the preceding quarter. Despite an overall rise in pan-India absorption, the reduced share of the top ten micro-markets underscores increasing geographical diversification. This diversification can be attributed to enhanced intracity connectivity, ample availability of grade-A and sustainable office spaces, competitive rentals to minimize operating costs, and maturing residential localities nearby.

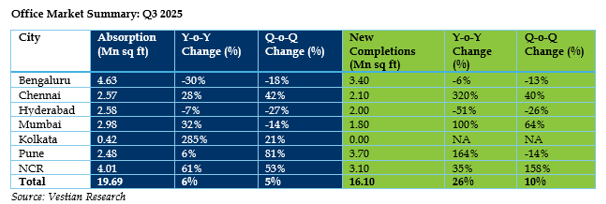

Robust GDP growth, controlled inflation, stable monetary policy, strong employment outlook, and high inflow of FDI & investments strengthened India’s real estate sector. Pan-India office absorption rose by 6% year-on-year and 5% compared to the previous quarter amid global macroeconomic uncertainties and geopolitical frictions, reaching 19.69 Mn sq ft. This marked the second-highest absorption level ever recorded, following the historic peak of 21.62 Mn sq ft in Q4 2024. Southern cities provided the thrust for this growth, with Bengaluru, Chennai, and Hyderabad together accounting for 50% of the pan-India absorption in Q3 2025.

Bengaluru continued to lead the pan-India absorption with 4.63 Mn sq ft in Q3 2025, followed by NCR at 4.01 Mn sq ft and Mumbai at 2.98 Mn sq ft. Kolkata recorded the lowest absorption of 0.42 Mn sq ft in Q3 2025, yet registered a 21% quarter-on-quarter and 285% year-on-year increase, primarily due to a low base effect.

IT-ITeS sector accounted for 31% of the total absorption reported in Q3 2025, registering a sharp decline from nearly 50% in Q2 2025. Meanwhile, BFSI sector’s share more than doubled to 15% from 6% during the same period, underscoring growing occupier interest from financial institutions. The share of Flexible Spaces remained stable at 14% compared to the previous quarter.

As absorption increased, construction activity also rose in Q3 2025, with new completions reaching 16.1 Mn sq ft — 10% quarterly and 26% annual surge. The increase in supply was largely driven by project completions in Pune, Bengaluru, and NCR, which together contributed 63% of the total new completions across the top seven cities. Pune led new supply additions with 3.70 Mn sq ft, accounting for 23% of the pan-India supply, followed closely by Bengaluru with 3.40 Mn sq ft (21% share). Chennai witnessed an annual increase of 320% in new office supply, driven by a low base effect. The city added 2.10 Mn sq. ft. of new office space—its highest supply addition in the past seven quarters.

Mr. Shrinivas Rao, FRICS, CEO, Vestian said, “The third quarter of 2025 reported the highest absorption of the current year, primarily driven by GCCs. This robust demand kept the office market buoyant amid global trade uncertainties and geopolitical tensions. Construction activity also gained momentum, with significant supply additions across the key markets. Robust absorption, healthy supply, and a diversified occupier base are expected to drive the next wave of growth in the coming quarters. H-1B visa restrictions may further amplify the demand for offices in India as more and more GCCs expand their footprint in India.”

.png)