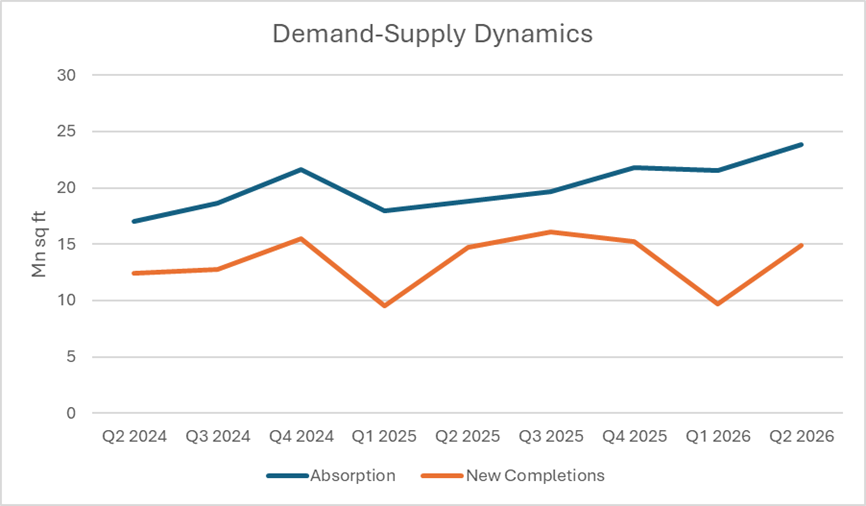

Construction activity rebounded in Q2 2026 after a subdued previous quarter, while office leasing grew at a much faster pace. This can be substantiated by the fact that new completions increased by 53% quarter-on-quarter to 14.9 Mn sq ft, while absorption reached an all-time high of 23.9 Mn sq ft, widening the demand-supply gap to 9.0 Mn sq ft in Q2 2026 as per Vestain report. As a result, vacancy levels improved by 105 basis points and rentals appreciated in the range of 3-9% over the previous year. The gradual widening of the demand supply gap is expected to further reduce vacancy levels and drive rental appreciation across major commercial hubs, indicating a gradual shift towards a developer-driven market.

Source: Vestian Research

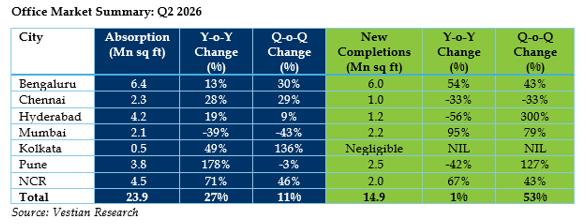

The recovery in construction activity was primarily led by Bengaluru, Pune, Mumbai, and NCR, which together accounted for nearly 85% of the total new completions during the quarter. Bengaluru alone contributed 40% to the pan-India supply, reflecting developers' continued focus on established office markets.

On the demand side, leasing activity remained concentrated in India's key business hubs, with Bengaluru, NCR, and Hyderabad collectively accounting for around 63% of the pan-India absorption in Q2 2026. Southern cities - Bengaluru, Chennai, and Hyderabad - contributed 54% to the total leasing, up from 49% in the previous quarter. In contrast, the share of Western cities declined from 35% to 25% during the same period, largely due to a temporary moderation in leasing activity in Mumbai.

IT-ITeS continued to dominate office demand with 41% share of the total absorption during the quarter. Managed Offices/Coworking/Flexible Spaces remained the second-largest occupier category with 22% share, reflecting occupiers' growing preference for agile workplace solutions. Notably, Flex Space operators ranked among the top two occupier segments across all major cities and even emerged as the largest occupier in NCR. Meanwhile, BFSI accounted for 8% of the total leasing, supported by the continued expansion of financial institutions.

GCCs remained the major demand driver of office demand, leasing 12.5 Mn sq ft and accounting for 52% of the total absorption during Q2 2026. Bengaluru, Hyderabad, and Pune together accounted for 72% of the overall absorption by GCCs, reaffirming India's position as the preferred destination for multinational corporations establishing Global Capability Centres (GCCs). The sustained expansion of GCCs, coupled with occupiers' growing preference for sustainable workplaces, resulted in green-certified office buildings accounting for 87% of the total leasing during the quarter, up from 85% in Q1 2026.

Consequently, vacancy levels improved across all seven major cities, with NCR and Kolkata recording the sharpest decline of 189 basis points each over the previous quarter, while rentals witnessed marginal appreciation across major office markets. Vacancy may further improve, and rentals are expected to rise in the future due to the rising demand-supply gap in the market.

Shrinivas Rao, FRICS, CEO, Vestian said, “India’s office market continued its growth momentum in Q2 2026 on the back of strong occupier demand. To cater to the rising demand, developers ramped up construction activities across the major cities, resulting in significant supply additions and new project launches in Q2 2026. The continued expansion of Global Capability Centres (GCCs), along with sustained demand from technology companies and managed office and flexible workspace operators, is expected to keep the office market buoyant in the future as well.”

City-wise Analysis

- Bengaluru: Retained its leadership position, accounting for 27% of the pan-India absorption, with ORR contributing to 76% of the city's leasing activity.

- Chennai: Technology and Flex Space occupiers continued to drive leasing activity, while the city maintained one of the lowest vacancy rates among the top seven office markets at 3.4%.

- Hyderabad: PBD-West dominated the market, accounting for 96% of the city's absorption, while GCCs continued to contribute 21% to the pan-India absorption by GCCs.

- Mumbai: The city recorded an absorption of 2.1 Mn sq ft in Q2 2026, the lowest in the past 12 quarters. BFSI remained the largest occupier with 36% share of the city's absorption.

- Kolkata: Leasing activity more than doubled over the previous quarter, with PBD accounting for 96% of the city's total absorption.

- Pune: Recorded the highest year-on-year growth (178%) in absorption among the top seven cities, supported by strong demand from Technology companies and GCCs.

- NCR: Emerged as the second-largest office market during the quarter, with Gurugram contributing 67% to the city's absorption, driven by robust demand from Flex Space operators.

India's office market continued to witness growth, supported by strong occupier demand and improved construction activity across major cities. Demand remained ahead of new supply, leading to lower vacancy levels and steady rental growth. Leasing activity was driven by sectors such as technology, Global Capability Centres (GCCs), and flexible workspaces, while developers continued to launch new office projects to meet future demand. With occupier confidence remaining strong and businesses expanding their office footprint, the commercial real estate market is expected to maintain positive momentum in the coming quarters.