According to Savills India's latest report, India's premium residential market remained broadly balanced during H1 2026, with average capital values across key cities continuing to record year-on-year appreciation. This momentum was driven by higher construction costs arising from elevated crude oil prices and supply chain disruptions triggered by geopolitical conflicts. At the same time, sustained demand from affluent homebuyers, HNIs, NRIs, entrepreneurs and corporate professionals, alongside a strong preference for branded, amenity-rich developments continued to underpin market performance.

The sector's underlying strength is particularly notable amid heightened global economic uncertainty characterised by geopolitical tensions and evolving trade dynamics. Against this backdrop, India's robust economic fundamentals, ongoing infrastructure development, well-supported financial system and sustained domestic wealth creation have reinforced investor confidence, positioning premium residential real estate as a preferred long-term investment for both domestic and NRI buyers.

The favourable macroeconomic backdrop supported capital value appreciation across residential segments. Under construction premium properties recorded consistent price growth, with annual average capital values rising across prime residential markets. Mumbai witnessed a 10-15 % YoY increase, while NOIDA witnessed an increase of around 4-28% YoY, Gurugram registered an increase of approximately up to 2% YoY, and Bengaluru witnessed capital value increase at around 3-11% YoY. The upward trajectory of this segment highlights sustained demand for modern and future-ready developments in well-connected growth corridors. It also reflects a market that is transitioning from rapid repricing towards more sustainable value creation, supported by premiumisation, rising incomes, calibrated supply and an enduring preference for quality.

Further, completed premium homes/luxury floors exhibited divergent trends across key residential markets. Annual average capital values increased by 10–25% YoY in Delhi, 8–10% in Bengaluru, 2–7% in Mumbai, and 2-6% YoY across micromarkets in Gurugram, except Golf Course Road recording a marginal dip of 2% YoY. The appreciation was supported by limited ready inventory, strong preference for immediate possession, and improving rental fundamentals across prime residential locations. In contrast, NOIDA registered a dip of around 2% YoY averaging at city level, driven by price normalisation.

Moreover, premium residential rental trends remained buoyant, with average rental values recording a rise across key cities, driven by sustained demand for quality ready homes, limited inventory of completed properties and a continued preference for well-connected, lifestyle-led developments.

While India's residential market remains fundamentally robust, the pace of appreciation has naturally become more measured as buyers evaluate properties more selectively. Buyers are increasingly prioritising quality, location and developer track record over speculative price gains. This reflects the evolution of the luxury residential market into a more institutionalised and mature asset class.

Shveta Jain, Managing Director, Residential Services, Savills India said, "India's premium residential market continues to witness resilient capital value growth, underpinned by strong fundamentals rather than rapid price escalation. Buyer preferences are becoming increasingly discerning, with greater emphasis on location, product quality and developer credibility, signalling a shift towards quality-led demand. While select micromarkets have seen marginal price corrections, these largely represent price normalisation within an otherwise balanced market. Looking ahead, we expect the market to sustain measured price appreciation, with premium residential real estate remaining a preferred long-term asset class, supported by disciplined pricing, calibrated supply and buyers' inclination toward premium residential properties.”

The report further delves into the key trends these cities witnessed through the year;

Mumbai

- During H1 2026, Mumbai witnessed an average 2-7% YoY rise in capital values for completed properties and a 10-15% YoY increase for under-construction properties within the premium segment.

- Demand remained steady across the premium and luxury segments, driven by end-users seeking larger residences, superior product specifications, and amenity-rich developments. Developers continued to focus on differentiated offerings, including spacious configurations, wellness-centric amenities, and integrated lifestyle features, supporting premium pricing for new launches.

- Infrastructure-led locations such as Thane, Navi Mumbai and the Central Suburbs continued to witness healthy demand and steady capital value growth, supported by improving connectivity through Metro corridors and the Mumbai Trans Harbour Link (MTHL).

- The ultra-luxury segment continued to witness healthy demand, particularly in prime micromarkets such as Worli, Prabhadevi and South Mumbai, supported by limited supply and sustained buyer interest in premium developments.

Bengaluru

- Average capital values of Bengaluru's premium residential properties continued an upward trajectory during H1 2026, supported by sustained demand for premium amenity rich properties, new launches of premium properties, ongoing infrastructure investments, and limited ready inventory across key premium residential corridors.

- Under construction premium properties recorded 3–11% YoY average capital value appreciation, driven by improving buyer confidence in newly launched developments, premium product positioning, and developers' calibrated pricing strategies. In comparison, completed properties registered a relatively firm yet robust 8–10% annual price increase, supported by strong demand and preference by end-users and investors for ready assets.

- East and North Bengaluru emerged as the leading corridors in terms of price appreciation for under construction luxury properties, registering around 8–11% YoY growth. The increase was supported by sustained residential demand, expanding commercial ecosystems, and continued infrastructure upgrades across key hubs such as Whitefield, Sarjapur Road, HSR Layout, Thanisandra, Hebbal and Yelahanka.

- Central Bengaluru continued to command the highest average capital value among completed residential properties, registering around 9–10% YoY growth, driven by its established premium residential profile, limited new supply, and sustained demand for well-located ready homes. Meanwhile, East, North, and South Bengaluru recorded a balanced appreciation of approximately 8–9%, driven by expanding residential catchments, improving infrastructure, and steady demand from both end-users and investors.

Delhi

- Average capital values of luxury floors in Delhi rose 15% YoY at the city level in H1 2026, driven by sustained demand for larger 3 and 4-BHK configurations with private terraces, dedicated parking, and home automation features.

- Among micromarkets, South-Central led price growth with a 25% YoY increase in independent floor values, as compared to a 9% annual increase recorded in H1 2025. Central-1 followed with 14% growth, while Central-2 and South-West each registered 13% annual appreciation.

- Average plot values in Delhi increased 6% YoY at the city level in H1 2026, moderating slightly from 7% annual growth registered in H1 2025. South-West led with 12% annual growth, followed closely by South-Central at 11%, underscoring steady demand for land in established residential pockets.

Gurugram

- Average capital values for completed luxury properties in Gurugram registered a 2% YoY growth at the city level in H1 2026. Among the micromarkets, Dwarka Expressway led with a 6% YoY increase, followed by New Gurugram and GCER & SPR with 3% and 2% annual appreciation, respectively.

- At the city level, all the micromarkets in the under-construction segment saw a marginal YoY appreciation of less than 2%.

- Capital values of residential plots continued to rise, averaging 11% annual growth citywide. Dwarka Expressway stood out at 16% YoY growth, while GCER & SPR and New Gurugram each recorded 12% annual appreciation, driven by limited land supply and steady investor demand.

NOIDA

- Capital values for completed luxury properties in NOIDA saw a 2% YoY decline on average, at the city level, in H1 2026, reflecting a phase of price normalisation after several years of consistent growth. The NOIDA–Greater NOIDA Expressway remained the most stable, posting a 3% annual gain, while capital values in Sector 150 and NOIDA Others witnessed 7% and 3% declines, respectively.

- Under construction properties held up better, with average capital values at the city level rising 15% on an annual basis. At the micromarket level, NOIDA-Greater NOIDA Expressway led with a 28% YoY increase, followed by Sector 150 and NOIDA Others at 13% and 4% annual growth, respectively.

North Goa

- North Goa's residential market continued to witness a modest correction in capital values during H1 2026, with prices softening by 4–6% YoY across micromarkets. The moderation reflects a gradual market recalibration following the sharp appreciation witnessed over the past few years, when strong demand from second-home buyers, HNIs, and investors had driven capital values to elevated levels.

- Residential plots in the 250-350 sq. m. category continue to account for a significant proportion of unsold inventory across both primary and secondary markets, highlighting a persistent demand-supply mismatch. As a result, many developers have adopted more flexible pricing strategies to accelerate sales, exerting downward pressure on capital values.

- Residential demand continued expanding beyond established coastal hubs into emerging locations such as Moira and Nerul, driven by buyers seeking lower-density living, larger plots at relatively affordable prices.

- The operational Manohar International Airport at Mopa, along with the Zuari Bridge, has significantly enhanced regional connectivity and local connectivity by improving access between North and South Goa and reducing travel times to key tourism and residential destinations. These infrastructure upgrades have strengthened the appeal of established micro-markets while also unlocking the potential of emerging residential corridors, encouraging both end-users and second-home buyers to explore new locations.

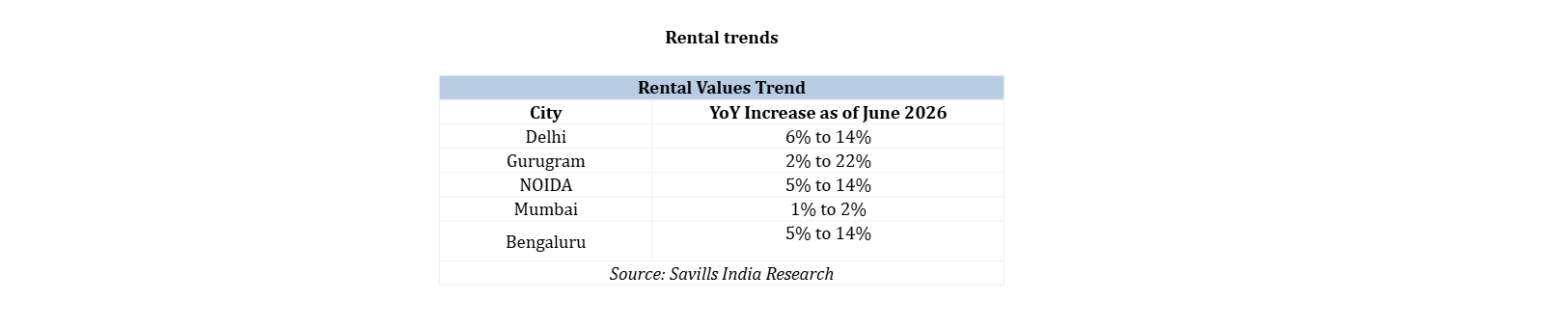

Rental Trends

Mumbai

- During H1 2026, Mumbai witnessed a 1–12% YoY increase in average rental values across premium residential micro-markets, supported by steady leasing demand for larger homes in amenity-rich developments.

- The rise in rental values can be partly attributed to pent-up demand for rental properties due to redevelopment of dilapidated buildings in the city.

- Residential properties located near key infrastructure such as Metro Line 3, the Coastal Road and the Mumbai Trans Harbour Link (MTHL) witnessed stronger leasing activity and rental growth, particularly across Central Mumbai, Western Suburbs, Navi Mumbai and Thane.

Bengaluru

- Citywide rents surged by around 5–14% YoY in H1 2026, driven by sustained demand for premium ready homes, limited availability of high-quality completed inventory, and a growing buyer preference for renting luxury residences before making long-term purchase decisions. The segment also continued to benefit from increasing participation from affluent domestic buyers and NRIs, supporting rental value growth across established micromarkets.

- Central Bengaluru led rental appreciation by around 14% YoY, reflecting the enduring appeal of its established luxury neighbourhoods, where stringent supply additions, and the exclusivity of premium residential inventory in locations such as Richmond Road and Cunningham Road continued to support rental premiums.

- East Bengaluru followed with nearly 12% YoY appreciation, underpinned by the maturity of its premium residential ecosystem, increasing concentration of high-end gated developments, and sustained preference for lifestyle-oriented communities with comprehensive amenities.

- North and South Bengaluru witnessed strong rental momentum, supported by the rapid expansion of premium residential communities, improving lifestyle and social infrastructure, and increasing preference among affluent households for larger residences within integrated townships and amenity-rich gated developments. The availability of contemporary luxury housing, coupled with evolving lifestyle preferences, continued to strengthen rental demand across these micromarkets.

Delhi

- Delhi’s luxury rental market moderated to 10% YoY growth, averaging at the city level from 34% annual appreciation in H1 2025

- South-Central continued to outperform with 14% annual appreciation in average rentals, followed by Central-1 micromarket with 10%, South-East micromarket with 9%, and South-West micromarket with 6% rental appreciation.

Gurugram

- Gurugram's average rentals, at the city level, witnessed 10% YoY growth in H1 2026.

- Dwarka Expressway showed an impressive 22% annual appreciation, followed by Golf Course Road with an 11% YoY rise. GCER & SPR and New Gurugram witnessed marginal 2-3% growth YoY.

NOIDA

- Average rentals grew by 10% YoY at the city level in comparison to 7% YoY increase in H1 2025.

- NOIDA Others recorded the highest annual rental growth at 14%, followed by the NOIDA–Greater NOIDA Expressway at 9% YoY, driven by rising demand for rental housing as the expanding corporate presence along the expressway corridor continues to attract a larger workforce.

New launches across key cities:

- Bengaluru witnessed a robust 56% YoY increase in premium residential launches in H1 2026, with around 13,094 new units entering the market.

- Launch of new luxury apartments in Gurugram declined by 28% YoY, with approximately 4,549 units launched in H1 2026.

- NOIDA saw the launch of approximately 400 luxury units, reflecting a 33% YoY decrease from H1 2025 levels

India's premium residential market is expected to remain resilient, supported by strong economic fundamentals, infrastructure expansion, urbanisation, and sustained demand from end-users and long-term investors. Going forward, the market is likely to witness measured and sustainable price appreciation, with buyers increasingly prioritising quality, location, lifestyle offerings, and developer credibility. Developers are also expected to maintain a calibrated approach to new launches, ensuring a balanced demand-supply environment and supporting the long-term growth of the premium housing segment.