5 key highlights from the 2025 India Vestian office market report:

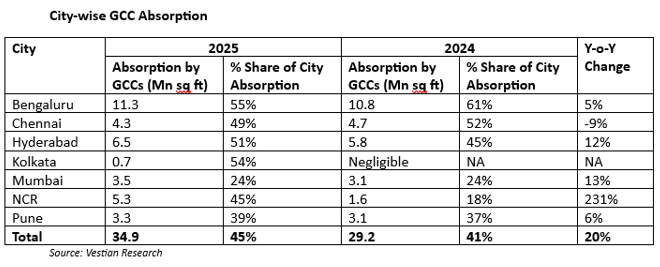

- GCCs Drive Growth – Global Capability Centres (GCCs) led the office market, accounting for 45% of pan-India absorption (34.9 Mn sq ft), up from 41% in 2024, marking a 20% YoY increase in GCC-led absorption.

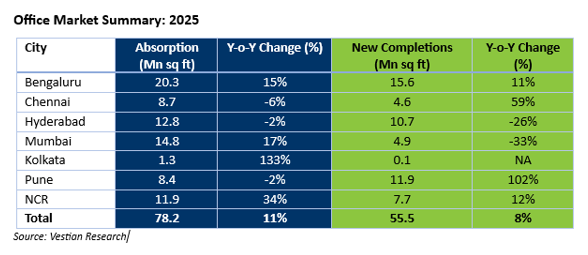

- Record Office Absorption & Supply – Pan-India office absorption reached an all-time high of 78.2 Mn sq ft, up 11% YoY. Developers responded with record new completions of 55.5 Mn sq ft, an 8% increase, highlighting strong demand-supply activity.

- Vacancy Levels Improve – Pan-India vacancy rates dropped sharply from 13.9% to 10.8%, with improvements across all major cities except Pune, reflecting robust leasing momentum.

- Sectoral Diversification – IT–ITeS dominated leasing (38% of absorption), but BFSI and flex spaces each contributed 14%, indicating growing depth and diversification in office demand. Over half of IT–ITeS leases were GCC-led.

- City-wise GCC Concentration – Bengaluru led with 32% of total GCC absorption, followed by Hyderabad (19%) and NCR showing sharp growth (18% → 45%), highlighting rising prominence of emerging cities as GCC hubs.

Global Capability Centres (GCCs) emerged as the primary growth driver of India’s office market in 2025, accounting for 45% of the total pan-India absorption, up from 41% in 2024. In absolute terms, GCC-led absorption reached 34.9 Mn sq ft, registering a 20% year-on-year increase.

Strong demand from GCCs, supported by a favourable policy environment and restrictions on the H1-B visa, propelled pan-India office absorption to an all-time high of 78.2 Mn sq ft in 2025. Despite ongoing global macroeconomic uncertainties and geopolitical headwinds, total absorption recorded an 11% year-on-year growth, underscoring the resilience of India’s office market.

To meet rising demand, developers accelerated construction activity across major markets. Consequently, new completions increased by 8% to 55.5 Mn sq ft, marking the highest annual supply ever recorded in a calendar year.Vacancy Levels Improve Sharply

Office absorption continued to outpace new supply by a wide margin in 2025, leading to a notable improvement in occupancy levels. The pan-India vacancy rate declined by 310 basis points, from 13.9% in 2024 to 10.8% in 2025.

Vacancy levels improved across all major cities except Pune, where vacancies increased by 4.6% due to significant supply additions of 12 Mn sq ft during the year. Across other markets, vacancy corrections ranged between 0.1% and 5.9%, reflecting healthy demand-supply dynamics.

Sectoral Diversification Strengthens Market Depth

IT–ITeS sector continued to dominate leasing activity, accounting for 38% of the total absorption, followed by BFSI and flex spaces, each with 14% share. This trend highlights increasing sectoral diversification in office demand.

Notably, over half of the IT–ITeS occupiers leasing office space in 2025 were GCCs. In value terms, GCCs contributed to nearly 60% of the total area transacted by the IT–ITeS sector, reaffirming their central role in market expansion.

Bengaluru dominated with 32% share of the total area absorbed by GCCs in 2025, followed by Hyderabad with 19% share. NCR witnessed a sharp rise in GCC activity, with the share of area absorbed by GCCs increasing from 18% in 2024 to 45% in 2025, reinforcing its growing prominence as a global GCC destination.

Despite global uncertainties, 2025 emerged as a landmark year for India’s office market, registering the highest-ever absorption and new completions in a single calendar year. Sustained demand from GCCs, robust economic growth, and a growing preference for Grade A and green-certified office spaces kept leasing activity strong across major cities. While IT-ITeS sector continued to dominate demand, increased participation from BFSI, healthcare, engineering, and flex operators has added depth and resilience to the market.

Outlook: Continued Momentum Ahead

Office absorption has demonstrated a consistent upward trajectory, increasing from 61 Mn sq ft in 2023 to 70 Mn sq ft in 2024, and reaching nearly 80 Mn sq ft in 2025. At the current pace, absorption is expected to rise further to 85–90 Mn sq ft by the end of 2026.

This growth is expected to be driven largely by sustained GCC demand. The share of GCCs in total absorption has expanded from 41% in 2024 to 45% in 2025 and is projected to exceed 50% by 2026, supported by expanding adoption across BFSI, healthcare, engineering, R&D sectors, alongside technology-led demand.

.png)