India’s residential real estate market recorded housing sales of over 6.14 lakh units worth ₹8.46 lakh crore in 2025, highlighting continued strength in the sector despite moderation in overall transaction volumes. The data comes from a joint report released by the Confederation of Real Estate Developers' Associations of India (CREDAI) and property research firm Liases Foras.

While the number of homes sold declined slightly from the previous year, the overall value of residential transactions increased by about 16% compared with 2024, indicating a clear shift toward higher-priced housing across urban markets. The report, which analyses residential activity across 50 major cities, suggests that India’s housing market is increasingly being driven by the premium segment.

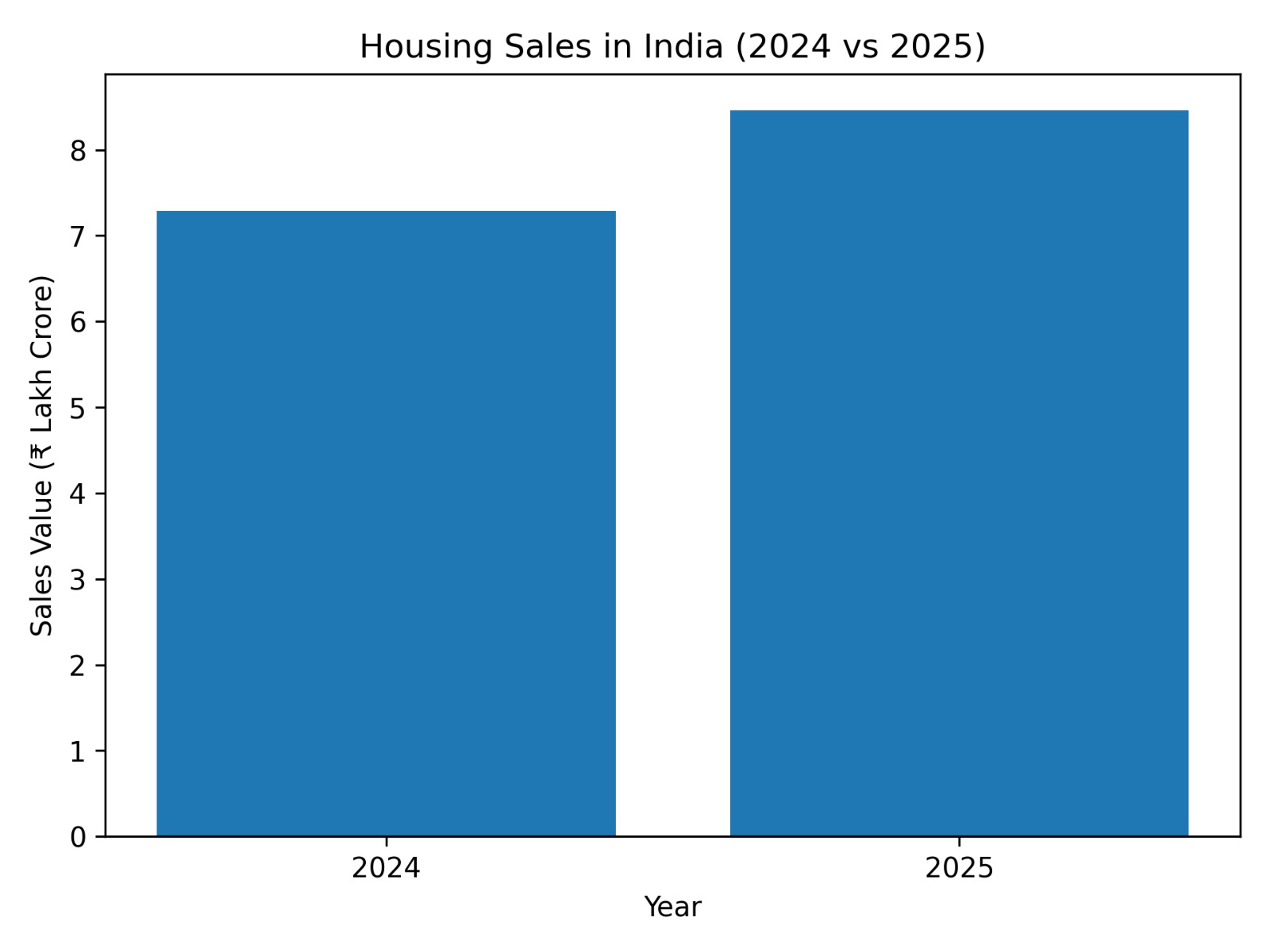

Source: Confederation of Real Estate Developers' Associations of India (CREDAI) & Liases Foras report

Source: Confederation of Real Estate Developers' Associations of India (CREDAI) & Liases Foras report

Total housing sales value across 50 Indian cities rose from ₹7.29 lakh crore in 2024 to ₹8.46 lakh crore in 2025, reflecting a sharp increase in premium and high-value residential transactions.

Premium Homes Dominate Market Value

Homes priced above ₹1 crore accounted for roughly 78% of the total sales value recorded in 2025, underlining the growing share of high-ticket residential transactions. Within this segment, ultra-luxury homes priced above ₹2 crore contributed more than half of the total sales value, reflecting rising demand from affluent buyers and investors.

The trend points to a broader shift in buyer preferences toward larger homes and upgraded residential developments, particularly in urban centres where household incomes and investment appetite have strengthened.

Major Cities Lead Residential Activity

Most housing sales were concentrated in large metropolitan markets including Mumbai, Hyderabad, Gurugram, Bengaluru, Noida and Pune. Among these, Mumbai recorded the highest sales value, supported by strong demand for premium and luxury residential projects. Other major markets also saw steady activity, reflecting sustained demand in employment-driven urban centres.

Developers have increasingly focused on projects in the mid-to-premium segments in recent years, responding to demand from high-income households and investors.

Supply Pipeline and Inventory

The report notes that new residential launches across the 50 cities stood at around 4.99 lakh units in 2025, while unsold inventory was estimated at about 9.63 lakh units.

These figures indicate relatively balanced market conditions, with supply remaining aligned with demand in most major urban centres.

Outlook for the Housing Sector

The data suggests that India’s housing market is undergoing a structural shift where transaction values are rising faster than sales volumes. This change is largely being driven by premium housing demand and increasing property prices across major cities.

Industry observers say continued urbanisation, infrastructure development and rising investor participation are likely to sustain demand in the premium and upper-mid housing segments in the near term. However, the trend also highlights a widening gap between premium housing demand and the supply of affordable homes, a challenge that continues to shape India’s residential real estate market.

.png)