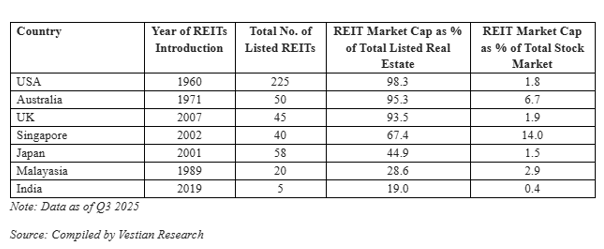

India’s Real Estate Investment Trust (REIT) market remains at a nascent stage, with REITs accounting for only 19% of the country’s listed real estate value, compared to a global average of 57%. While this gap highlights India’s relative under-penetration, it also signals substantial headroom for long-term growth as the market matures and diversifies, according to Vestian Research.

India currently has five listed REITs, four focused on office assets and one in the retail segment. The dominance of office REITs reflects the early stage of the ecosystem, as most other real estate asset classes are yet to achieve the scale, maturity, and institutional structure required for public REIT listings.

Global REIT Landscape: A Sharp Contrast

Globally, the REIT ecosystem is much more diversified in nature. The ecosystem in the US, Australia, Singapore, Japan, and the UK comprises a range of different REITs, including residential, healthcare, logistics, self-storage, data center, and mortgage-backed REITs. In the US and Australia, more than 95% of the total securitized real estate market exists in the form of REITs, which reveals the maturity of the respective markets.

By comparison, the total Indian REIT market capitalization is a mere 0.4% of the overall stock market; this is sufficient confirmation of the nascent stage of the industry in the Indian scenario, and the huge potential that lies untouched in this sector

India’s REIT Ecosystem: Early but Expanding

Although REIT regulations were notified in 2014, India’s first REIT listing came only in 2019. Over the past six years, the sector has grown rapidly, expanding from INR 264 billion in FY20 to INR 1.6 trillion by Q2 FY26. However, the availability of stabilised, income-generating assets remains limited, as a large portion of commercial stock is either under construction or held in fragmented ownership structures.

Office Sector: The Backbone of Indian REITs

Office assets continue to anchor India’s REIT market, with listed portfolios spanning over 135 million sq ft. These assets benefit from predictable leasing demand from Global Capability Centres (GCCs), technology firms, and BFSI occupiers, supporting stable yields of 5–7%.

India has over 1 billion sq ft of office stock, of which nearly 500 million sq ft is considered REIT-worthy. An additional 34 million sq ft is already part of existing REIT pipelines. Developers are increasingly preparing to monetise this potential. Notably, Bagmane Developers, backed by Blackstone, is expected to launch an INR 4,000 crore REIT IPO in early 2026, which could become the next major listing and further deepen institutional participation.

Retail REITs: A Largely Untapped Opportunity

Retail REITs have been slower to emerge due to the sector’s dependence on footfall dynamics, consumption trends, and long-term tenant management. Currently, Nexus Select Trust is India’s only retail REIT, despite the country having over 89 million sq ft of Grade A retail stock.

Currently, there are merely 10.6 million sq ft of Grade A malls in REITs, while there is a potential for institutional-grade real estate almost eight times larger. With consumerism penetrating deeper and institutional-grade malls maturing, REIT-ready retail properties are likely to increase from INR 1.5 trillion in 2025 to INR 2.4 trillion in 2030. Industry analysts expect two to three retail REITs to be launched in the next three to five years. The market for the retail REIT industry may be USD 6-9 billion by 2030. Greenfield IndianTier II cities such as Indore, Coimbatore, Surat, Chandigarh, and Bhubaneswar also hold serious consideration here.Emerging Asset Classes: The Next Frontier

In addition to office spaces and shopping malls, other real estate categories like warehousing spaces, industrial parks, logistics hubs, and data centers are soon expected to trigger the next phase of growth in India’s realty mutual fund. The opportunities in industrial and warehousing REIT/InvIT could rise from INR 0.7 trillion in the current state to INR 1.3 trillion by the year 2030.

There is a lot of upside in the REIT market in India, as the penetration is low and the need is to diversify beyond offices and select retail real estate, stated Shrinivas Rao, FRICS, CEO, Vestian. He added that as the market develops, data centers, logistics real estate, industrial parks, and warehousing would provide scalable and yielding investment opportunities in line with models seen in more evolved international REIT markets."

In fact, Rao further clarified that the outlook for residential REITs still faces some difficulties in terms of low rental yields and existing policies, although some innovation in the form of rental housing could improve them. Additionally, he emphasized the possible crucial role that SM REITs could take in contributing to the development of the Indian REIT market through the pooling of smaller stabilized assets.

Residential Assets: Potential, Not Yet Prepared

Housing property is at the threshold of being covered under REITs. However, the property faces structural issues in the form of low yield on rentals at 2–3%, lack of segmentation in ownership, high tenant turnover, and the absence of large institutional rental assets. Moreover, the absence of a comprehensive rental housing policy in India is a key facilitator in mature markets such as the US, Japan, or Singapore. Emerging concepts such as co-living space, student housing, and senior living remain promising, although housing property as an REIT is still a longer-term opportunity.

Policy Support and SM-REITs

India’s regulatory framework is gradually evolving to support broader participation. The introduction of Small and Medium REITs (SM-REITs), allowing portfolios valued between INR 50–500 crore, marks a significant step towards democratising access. Structures such as PropShare Platina (2024) and PropShare Titania (2025) are already operational, with more expected as smaller commercial assets transition into formal, transparent vehicles.

The Indian REIT industry is growing from a state of infancy to adolescence. Marketisation is expected to rise from USD 18 billion in 2025 to USD 25 billion by 2030. The growth of REIT-ready office properties from INR 8.2 trillion to INR 16 trillion would double during the same period, and with this rise, other sectors like Retail REITs and alternative investment segments, India has a great prospect of becoming amongst the most vibrant REIT markets around the globe.

The building blocks are well set. The next stage of evolution will be fueled by the forces of diversification, scale, and focused policies—the key drivers which will help the India REITs evolve.