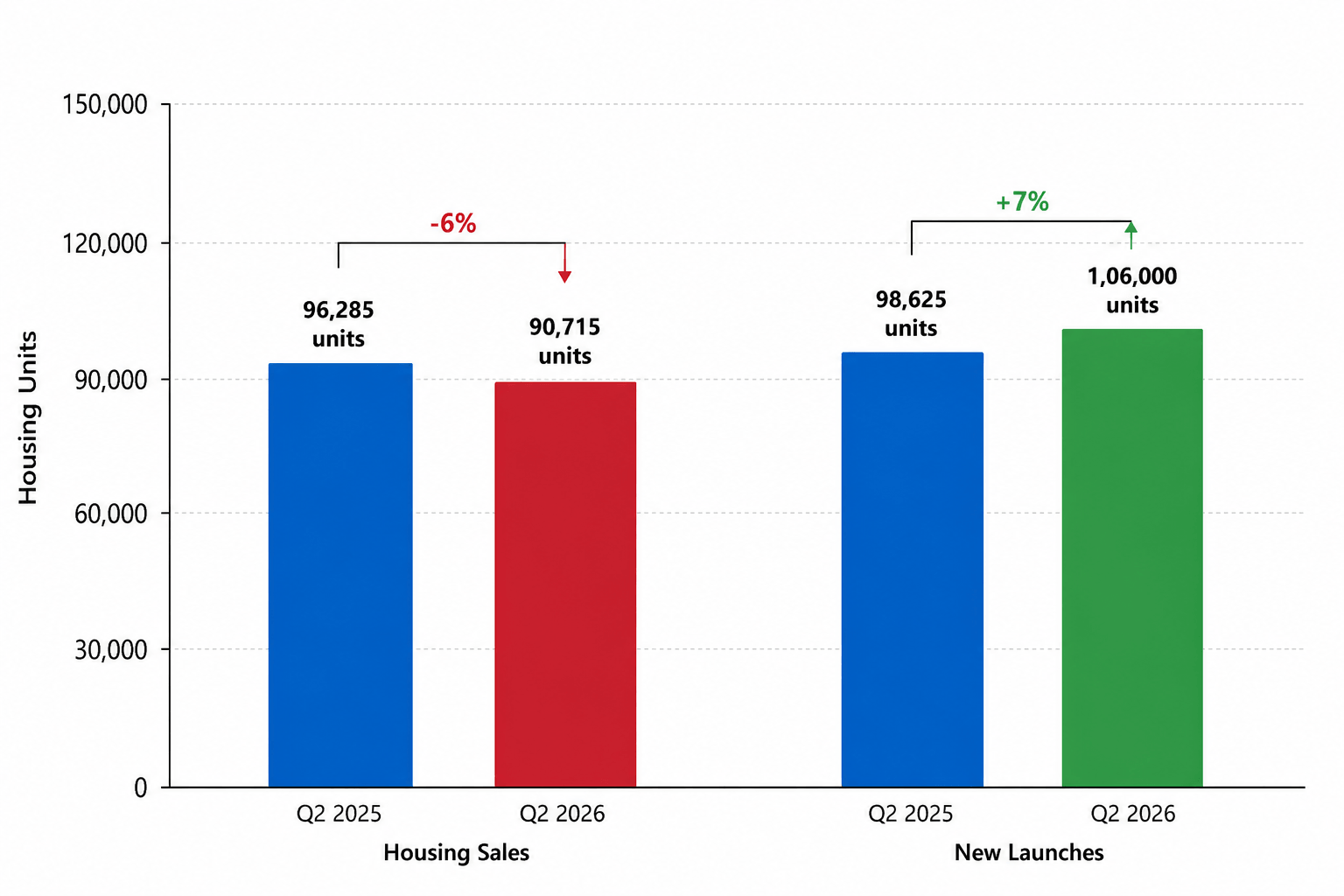

India's residential real estate market witnessed a moderation in the second quarter of 2026, with housing sales across the country's top seven cities declining 6% year-on-year as geopolitical tensions in West Asia and uncertainty surrounding the IT sector weighed on homebuyer sentiment. Despite softer demand, developers continued to expand supply, launching 7% more homes than a year ago, indicating long-term confidence in the sector, according to the latest ANAROCK Research report.

Residential sales stood at approximately 90,715 units during the April-June quarter (Q2 CY2026), down from 96,285 units in the corresponding period last year. On a quarter-on-quarter basis, housing absorption declined 11% from around 1.02 lakh units recorded in Q1 2026, marking the slowest quarterly sales performance since early 2023.

Developers Stay Bullish Despite Demand Moderation

While buyer activity softened, the supply side remained resilient. Developers launched nearly 1.06 lakh housing units during the quarter, a 7% annual increase over the 98,625 units launched in Q2 2025. However, launches declined 16% sequentially, indicating that developers have begun calibrating fresh supply in response to changing market conditions.

Source: ANAROCK Research, Q2 CY2026

According to Anuj Puri, Chairman, ANAROCK Group, the market is entering a more balanced phase after several years of exceptionally strong demand.

"These readings are along expected lines, as the Middle East war's impacts on the entire sector were all too obvious. What we have currently is a more balanced housing market where new supply is catching up with absorption as sales growth moderated across most top cities."

Puri added that Demand continues to remain strongest in premium housing, GCC-driven employment hubs, and infrastructure-led growth corridors, while disruptions arising from the West Asia conflict and AI-related uncertainty in the IT/ITeS sector have prompted some prospective buyers to postpone purchase decisions.

MMR and Bengaluru Continue to Lead the Market

The Mumbai Metropolitan Region (MMR) retained its position as India's largest residential market, recording approximately 28,710 housing sales during the quarter despite an 8% year-on-year decline. Bengaluru followed with around 15,285 units sold, registering marginal annual growth of 1%.

Together, MMR and Bengaluru accounted for nearly 48% of total housing sales and 53% of all new launches across the top seven cities, highlighting their continued dominance in India's residential market.

Kolkata Emerges as the Best Performer

Among the seven major housing markets, only three cities posted positive annual sales growth:

| City | YoY Sales Growth/fall |

| Kolkata | +10% |

| Hyderabad | +2% |

| Bengaluru | +1% |

| NCR | -6% |

| MMR | -8% |

| Chennai | -9% |

| Pune | -15% |

Premium Housing Continues to Dominate New Supply

The report highlights the continuing premiumisation of India's residential market.

Homes priced between ₹80 lakh and ₹1.5 crore accounted for the largest share (27%) of new launches during the quarter, followed by properties priced between ₹1.5 crore and ₹2.5 crore, which made up 25% of supply. Luxury homes priced above ₹2.5 crore contributed another 22%, while affordable housing (below ₹40 lakh) represented just 6% of total launches.

The shift underscores developers' continued focus on premium and upper-mid segment housing, where demand has remained relatively resilient.

Prices Continue to Rise; Inventory Builds Up

Even as sales moderated, residential prices remained firm.

Average housing prices across the top seven cities increased 7% year-on-year, although quarterly appreciation was limited to 1%. NCR witnessed the highest annual price growth at 13%, followed by Bengaluru at 8%.

Meanwhile, unsold housing inventory rose 10% annually to over 6.16 lakh units by the end of Q2 2026, reflecting the increase in project launches. Bengaluru recorded the sharpest inventory growth as developers accelerated new project additions.

Outlook: Market Remains Fundamentally Stable

While geopolitical developments temporarily dampened buyer confidence during the quarter, the continued rise in launches suggests developers remain optimistic about the medium- to long-term outlook for India's housing market.

Industry observers believe that healthy employment generation in GCC-led markets, expanding infrastructure projects, and sustained demand for premium housing are likely to support residential activity once geopolitical uncertainties ease. However, the pace of sales recovery will depend on global macroeconomic conditions, consumer confidence, and the evolving geopolitical landscape.