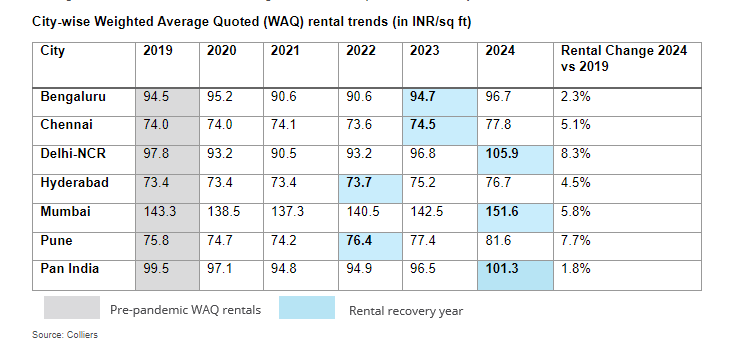

In the post-pandemic era, demand recovery in the office market has been swift, following a steep ‘V-shaped’ recovery trajectory. After subdued demand in 2020 & 2021, leasing activity had fully bounced back by 2022. In fact, since 2022, each year has been witnessing new all-time-high Grade A office space uptake at India level. With strong, consistent demand, average rentals have also surpassed the pre-pandemic levels (2019) across all the six major office markets for the first time in 2024. The rental recovery in the Indian office market, albeit relatively slower than the demand recovery trajectory has finally been fully complete, thus forming an elongated ‘U-shaped’ pattern.

Rental recovery pace varies across cities, surge highest in Delhi NCR and Pune

All throughout this recovery trail, certain cities such as Hyderabad and Pune achieved pre-pandemic rental levels in 2022 itself. While Bengaluru and Chennai breached 2019 rental levels in 2023, Delhi NCR and Mumbai completed the recovery cycle finally in 2024. Although Delhi NCR was amongst the last cities to breach pre-pandemic levels, the rental growth (2024 compared to 2019) has been the highest in Delhi NCR. In fact, Delhi NCR and Pune saw the highest rise in average rentals at about 8% each during the 2019-2024 period followed by Mumbai and Chennai with about 5-6% rise in the same period.

“Average rentals across all six major markets have breached pre-pandemic levels for the first time in 2024. Although the rental growth will vary across cities, annual increase in average quoted rentals at the end of 2024 is likely to be higher for certain cities like Delhi NCR and Pune as compared to other markets. Moreover, as demand scale-up in Indian commercial real estate solidifies, notwithstanding unforeseen events, annual space take up to the tune of 60 million sq ft is likely to be the new norm in the medium-term”, says Arpit Mehrotra, Managing Director, Office services, India, Colliers.

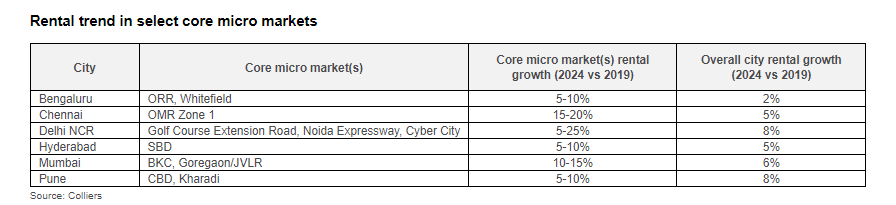

Rentals in core micro markets have outperformed city-level appreciation significantly

Interestingly, select core micro markets across the top six cities have witnessed up-to 25% rental growth during the 2019-2024 period. These micro markets have seen high demand across occupier segments, thus, witnessing higher rental growth compared to 2-8% city-level appreciation during the same period. Core micro markets in Delhi NCR such as Golf Course Extension Road, Noida Expressway and Cyber City have witnessed up-to 25% rise in rentals during the last five years. High activity micro markets of Bengaluru such as Outer Ring Road (ORR) and Whitefield have witnessed a surge of 5-10% as compared to the 2% city-level rental growth during 2019-2024 period. Similarly, office rentals in other core micro markets such as OMR Zone 1 in Chennai and Goregaon/JVLR & BKC in Mumbai too have surged by 10-20% from pre-pandemic levels, while average rental growth in respective cities has been comparatively lesser at 5-6%. Core micro markets are typically located in CBD and SBD areas of respective cities. The higher rental growth is reflective of occupiers’ preference for Grade A developments in localities that enjoy superior connectivity and are located in proximity of residential catchment areas.

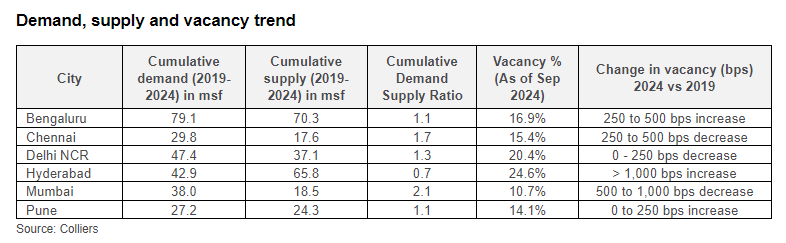

Cumulative office space demand in last 5 years has comfortably breached 250 msf

With continued strong momentum in the market, the six major office markets have already witnessed a cumulative Grade A office space demand of 264 million sq ft since 2019. Despite the demand blips in pandemic affected years, consecutive record-breaking leasing activity has helped in keeping the growth momentum intact. At an aggregate level, supply infusion has largely followed demand revival and is evident from the cumulative demand-supply ratio of 1.1 during 2019-2024. However, a city-level analysis of demand-supply contours throws interesting aspects. Mumbai, with a demand-supply ratio of 2.1, has witnessed a significant drop in vacancy levels since 2019, as demand has outpaced supply significantly. Similarly, in Delhi-NCR, with demand exceeding supply on a consistent basis, vacancy levels have dropped from around 25% a few years ago to about 20% currently. Hyderabad, on the contrary, has traditionally been a high-supply market and this has driven vacancy levels upwards constantly; current vacancy levels in the city are around 25%.

“After the initial years of the pandemic, occupiers and developers regained confidence in the office market of the country quite fast. Both demand and new supply in the last 5 years, especially in the post-pandemic era, have been quite impressive. Since 2019, cumulative demand and supply across the six major office markets of the country have been recorded at 264 and 234 million sq ft respectively. With overall demand and supply mirroring each other, vacancy levels are anticipated to be rangebound across most cities. Average office rentals meanwhile can further firm up and witness up-to 10% annual growth across key cities in 2024”, says Vimal Nadar, Senior Director & Head of Research, Colliers India.

The Indian office market has demonstrated a remarkable recovery post-pandemic, with average rents surpassing pre-pandemic levels for the first time in 2024. Demand for Grade A office space has remained strong, particularly in cities like Delhi NCR and Pune, which have seen significant rental growth. As cumulative demand and supply align, vacancy levels are stabilizing, indicating a robust market outlook, with expectations of continued rental growth across key urban centers.

.png)