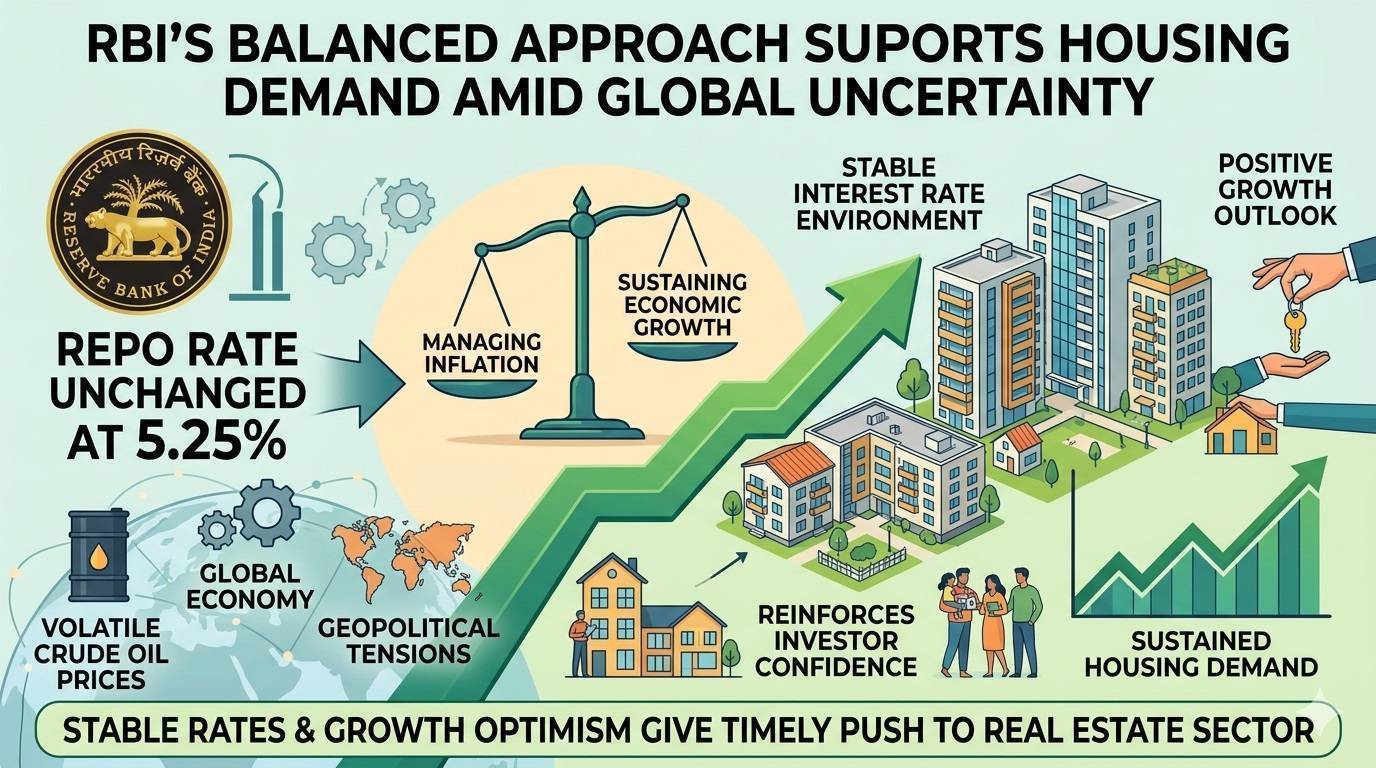

With the Reserve Bank of India (RBI) set to announce its monetary policy decision in August 2025, the real estate sector is bracing for cues that could influence both demand-side dynamics and project financing outlooks. Over the past quarters, India’s housing market has shown resilience amid inflationary pressures and elevated lending rates. However, developers and homebuyers alike are now watching for signs of a shift in the central bank’s policy stance, particularly in the lead-up to the crucial festive season when property sales typically surge.

While retail inflation has moderated within the RBI’s comfort range, real estate stakeholders remain concerned about sustained high borrowing costs. Home loan EMIs have remained high, especially for middle-income and first-time buyers, constraining affordability despite healthy income growth. Developers are also contending with increased input costs and delayed project cycles, making access to cheaper capital and more liquidity a pressing concern. Any shift in repo rates, stance, or regulatory easing will have a direct bearing on ongoing and upcoming residential launches.

Apart from repo rate expectations, the sector is also looking for broader signals related to liquidity for non-banking financial companies (NBFCs), credit growth, and refinancing terms. Large developers with established banking ties may weather the cycle, but smaller builders continue to face challenges in securing funding under tight monetary conditions. The August policy, therefore, is being seen not just as a rate decision but as a directional indicator for the coming quarters—potentially impacting sentiment across metros and Tier II cities alike.

Industry Experts Opinion

Mr. Jetaish Gupta, Founder and Director, Adore Group

“The stakes are high in the coming MPC decision deal for both home buyers and developers. Home purchase activity driven by cheaper borrowing while the impact of recent repo rate cuts is yet to be fully transmitted with faster lowering of lending rates by public sector banks versus their private sector peers. Developers Forum said there is also a need for better and faster transmission to ensure that all the benefits of low policy rates will be available to both new as well as existing borrowers, in order to maximize its multiplier effect on housing demand and construction activity. Meanwhile, the measured policy that is calibrated towards an inflation targeting way assures so that a rebound isn't something based on speculative deluge. The industry will look at MPC's inflation projections and its liquidity stance for an outlook on the medium term, as well as how external risk management is being considered.”

Mr. Siddharth Maurya, Founder & Managing Director, Vibhavangal Anukulakara Pvt Ltd

“The August 2025 RBI MPC review isn't just a macroeconomic event for personal finance enthusiasts and households; it's a turning point for wallets in India. Another repo rate cut will come as a relief for millions of borrowers who have floating-rate mortgages and personal loans, in an environment of global headwinds. While even a halting in the rate cut cycle at current record low rates will keep EMIs affordable and drive credit demand as banks chase new loan clients. That might really resonate for families preparing to do some heavy shopping or trying to make ends meet during a holiday season that typically includes a little more spending. With the potential boost to recurring payments and digital transactions, consumers may also consider reviewing their EMIs, loan structures, cash flows and harness the monetary policy environment to increase their savings buffer or repay debt faster — or use it as an opportunity to steer toward new financial horizons deliberately.”

Mr. LC Mittal, Director, Motia Builders Group

“Optimism has been surrounding the sector ahead of the RBI MPC meeting following a firm housing demand and improved affordability backed by 100 bps rate cuts in cumulative this year. Builders aspire that one last small rate reduction or a pause could help in preserving the allure of home loans after witnessing significant increments, especially from first-time borrowers. Mumbai: Public sector banks are ahead of private lenders in passing on lending rate cuts but the expectation is for more transmission to happen, which could revive primary housing sales as well as developers to expand their loan books. Industry experts have emphasized the importance of stability and predictability from the MPC level that they say will help reinforce confidence in both residential and commercial investments.”

Mr. Annuj Goel, Chairman, Goel Ganga Developments

“Stakeholders in the space are beginning to see indications of a durable recovery, with inflation at multi-year lows and monetary policy increasingly becoming accommodating. Albeit August may see no rate cut itself, but robust buyer interest and high levels of loan disbursals are being driven due to the existing low-rate scenario. Consistent with the sector's vulnerability to credit costs, an environment of continued macroeconomic stability and cautious regulation is likely to give a leg-up to launches and project completions, especially in urban growth corridors. In the urban markets, developers are waiting for a clear picture on one affordability of homebuyers and second is economic trend. The messaging and guidance from the MPC will have far reaching implications on investments and purchases through segments, making this policy meeting among the most consequential for the industry across all times.”

Mr. Keshav Mangla, GM - Business Development, Forteasia Realty

“The August 2025 policy review, on one hand, is against subdued inflation but varied urban-rural demand and global trade unease. Both builders and proponents of affordable housing expect interest rates to either hold steady or be cut, if only just a little, to boost the economy. It has already benefitted due to the earlier rate reductions, resulting in more sales and higher share prices for top companies. Policy continuity is good, developers said they are wary of the global tariff outlook as well as price volatility in commodities and construction costs that can affect housing demand in the months ahead. This should boost the capacity to unlock more inclusive and resilient urbanization, while at the same time putting a premium on macroeconomic resilience that will force the country to support credit growth.”

Way Forward

As the RBI gears up for its August 2025 policy announcement, the real estate sector awaits signals that go beyond interest rates, focusing on liquidity access, credit transmission, and long-term financial stability. A neutral or mildly accommodative stance could maintain momentum in both residential sales and project development, especially in the mid-income and affordable segments. However, the full benefit of previous rate cuts hinges on quicker lending rate transmission and improved funding access for smaller developers. Policymakers are expected to balance inflation control with support for economic recovery, and their guidance on liquidity, NBFC health, and housing-linked credit will likely shape real estate strategies well into the festive and post-festive quarters.

.png)