Buying a home is a major milestone in life for many. It usually means that one is financially stable, thinking about the future and is proud of himself/herself. However, most of the buyers tend to focus on the basic price of the property and their monthly EMI, but actually, the true cost of ownership remains hidden to them. A simple purchase may turn into a financial nightmare very easily due to the addition of hidden charges.

In India, the real cost of buying a house can go up by 8% to 20% more than the listed price depending on such things as the location, the developer's policies and the construction phase. As these extra costs are either not explained properly at the time of the purchase or are slowly given to the buyer during the process, they may be a shock to the buyer who is not ready for them. Being aware of these costs beforehand is not only beneficial but necessary for making a secure and comfortable investment decision.

Why Do Hidden Property Charges Matter?

Most of the time, the price shown in brochures or real estate listings is the base price of the unit only. However, the final amount to be paid is the sum of a variety of factors, including statutory charges, builder-specific costs, financing expenses, and post-possession spending. These extra costs will actually have a great impact on your financial planning.

They decide the amount of money you need to have on hand initially, influence your loan requirements, and if not planned properly, can even change your lifestyle after purchase. Most importantly, they change the definition of affordable in terms of property buying.

Being aware of hidden costs allows you to:

- Plan your total investment realistically

- Avoid last-minute financial strain

- Negotiate more effectively with developers

- Ensure a smoother ownership journey

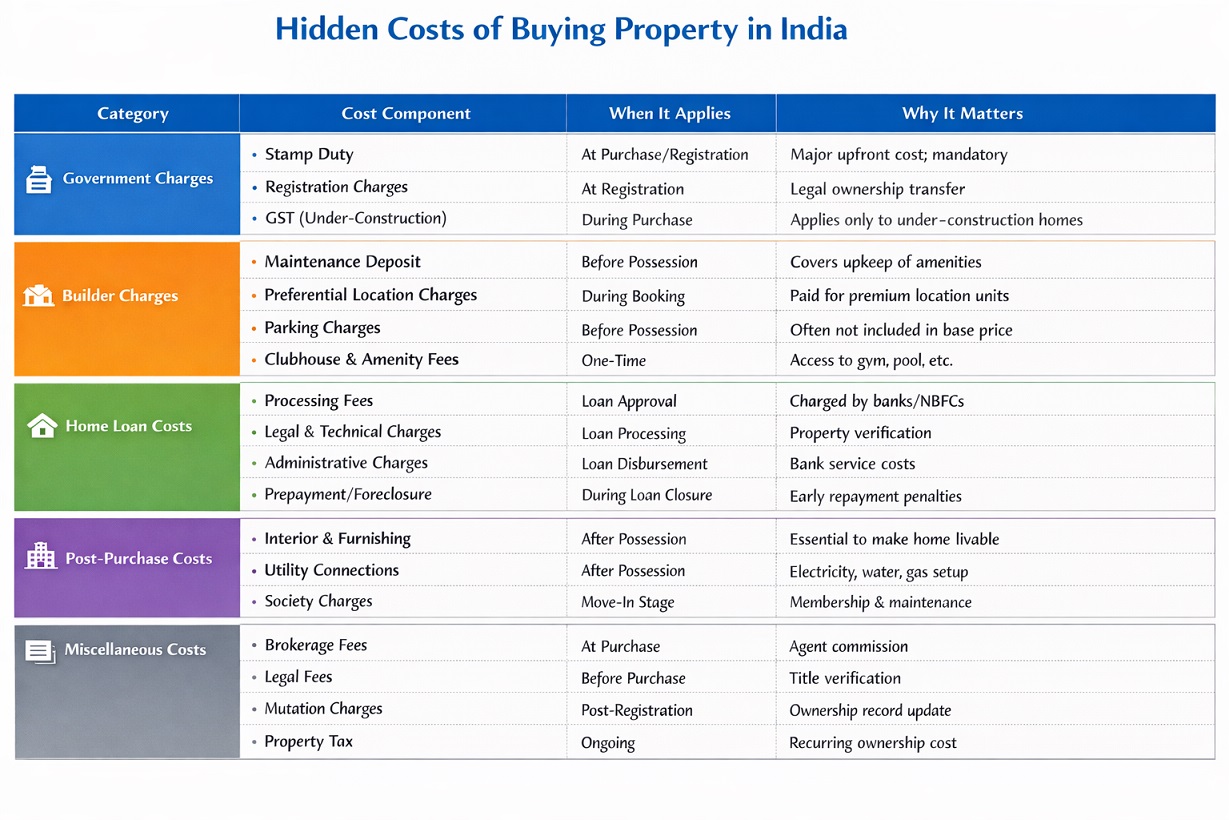

Government Charges: The Largest Mandatory Expense

One of the biggest chunks of untold cost comes from government mandated charges; these are non-negotiable and definitely required for legal possession . Such - charges will be one of the major components of your initial payment. Stamp duty is a state-level tax on property transactions and is usually between 4% and 8% of the property value.

For legal record purposes of the transaction, 1% registration fees are usually expected . The basis for calculating these government charges is either the agreement value or circle rate, whichever is higher, meaning that your tax liability could still be high even if you manage to negotiate a lower purchase price.

Builder-Imposed Charges That Increase the Final Price

Even though government fees are fixed, builders’ charges can vary a lot between projects and developers. These costs are often not clearly disclosed upfront, which can cause buyers to go over budget. Developers usually collect a maintenance deposit from buyers to fund high-quality amenities like lifts, security systems, and landscaped green areas.

There is also the matter of preferential location charges (PLC), These are usually levied only on units that have a better feature for instance, a park-facing apartment, a corner plot, or a unit closer to the main gate or recreational facilities. Like most sports, parking too has been fraught with issues for buyers who have not anticipated it in their initial budgets. On the contrary to popular belief, parking is not generally included in the base price but is sold separately. By the same token, if a buyer wants to have a club member's privileges of using the gymnasium, swimming pool, etc. a one-time fee usually has to be paid.

Common builder-related costs include:

- Maintenance deposit (advance)

- Preferential Location Charges (PLC)

- Parking charges

- Clubhouse and amenity fees

Home Loan Costs Beyond Interest Rates

Purchasing a house with the help of a loan will require the buyer not just to pay the loan interest but also additional expenses. Banks and other financial institutions generally charge a number of fees when a loan application is being processed and the loan is being given out. For instance, the processing fee for a home loan is charged at the rate of 0.25% to 1% of the loan amount and, besides that, banks usually perform legal and technical verification of the property which may result in separate fees.

At the same time, administrative charges can also be levied depending on the specific lender. Furthermore, to the extent that you may decide to repay the loan early, you may be subjected to prepayment or foreclosure charges. Nowadays, numerous lenders have softened such charges on floating-rate loans but it is still very necessary to check the conditions thoroughly.

Loan-related expenses include:

- Processing fees

- Legal and technical evaluation charges

- Administrative costs

- Prepayment or foreclosure charges (if applicable)

Post-Purchase Expenses That Are Often Underestimated

One of the biggest misconceptions buyers have is that their cost ends once the property is registered. However, the post-possession stage brings a whole different set of expenses that are just as important. Among the most costly items after the handover is interior furnishing.

Transforming a bare apartment to a delightful home requires investing in kitchens, wardrobes, lighting, and fittings. Depending on your choices, this can take up 5% to 10% of your total expenditure. Utility connections represent one more category of additional costs. Electricity, water supply, and gas pipeline installations are normally charged separately. Furthermore, housing societies may also require payment of membership fees, deposits, or transfer charges as part of the ownership process.

Post-possession costs typically include:

- Interior and furnishing expenses

- Utility connection charges

- Society deposits and membership fees

Other Costs That Are Easy to Overlook

Outside the main categories, there are quite a few other, smaller expenses that could affect your total budget. Such expenses are typically overlooked during planning session but at some point, they become tangible. Brokerage charges in case you buy through a real estate agent normally are around 1% to 2% of the property price. Likewise, the lawyer and paperwork charges become an issue if you hire a legal professional to check the property title and contracts. Similarly, mutation fees needed for recording the change of ownership in the local government offices and the yearly property tax are part of the cost of ownership of property. Whereas each of these expenses is small, taken together, they represent a significant part of the investment.

Tips to Stay Financially Prepared

To manage the hidden costs in an efficient way, a buyer needs to be proactive in his approach. If a buyer is prepared in advance, there are fewer chances of any financial surprises during the process.

Here are a few tips that can be followed to stay financially prepared:

- Request a detailed cost sheet

- Clarify what is included in the all-inclusive price

- Read all agreements before signing

- Maintain a buffer of at least 10-15% above the base cost

- Compare multiple builders and lenders before making a final decision

Purchasing a property involves more than just dishing out the sticker price; it requires one to be aware of the full monetary commitment. Hidden costs are a major aspect of real estate dealings in India. Unaware of these, one can be mishandled emotionally as well as financially. The best informed ones are buyers who evaluate each element of their cost layout thoroughly before deciding. Do not hasten into any agreement without first clearing your doubts by asking:

What is the total all-inclusive cost of this property? This simple query holds the key to emancipating you from the confusion and helping you confidently proceed utilizing information for your buying needs, coming to be a more rewarding experience.

Disclaimer: This article is for informational purposes only. Actual charges may vary depending on state regulations, builder policies, and individual circumstances. Always consult legal and financial professionals before making a property purchase decision.