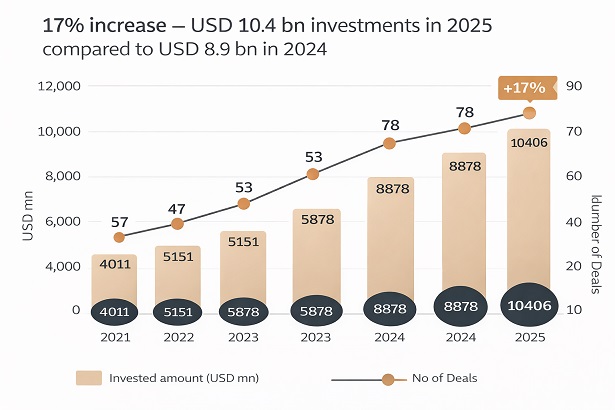

In 2025, the real estate sector in India attracted institutional investments worth $10.4 billion through 77 deals, according to data analysed by global property consultancy JLL. This was the highest-ever annual inflow into the sector and up a robust 17 per cent over the $8.9 billion invested in 2024. The performance makes 2025 the second successive year to witness record-breaking investments, thereby emphasizing the growing importance of India as an attractive destination for long-term investments in real assets.

Apart from the direct deals, the commitments on the platform level were recorded at $11.43 billion over a three-to-seven-year timeline. This commitment shows that the investors' faith in the Indian realty sector’s fundamentals is not driven by short-term trading.

Platform Deals Fuel Long-Term Capital Formation

One of the key characteristics of the year 2025 was the level of investment in platforms, with close to $11 billion from just one digital infrastructure investment platform. This is reflected in investment such as the joint venture between Reliance Industries and Brookfield Asset Management and Digital Realty Trust, doing business as Digital Connexion, to build data infrastructure in India. This deal proves the relevance of data centers and the digital infrastructure sector as an integral asset class, due to the exponential rise in the use of cloud, AI, and other digital consumption patterns in different sectors.

Domestic Capital Takes the Lead After a Decade

One of the most significant structural shifts in 2025 was the rise of domestic institutional investors, who accounted for 52 per cent of total real estate investments. This marked the first time since 2014 that domestic capital overtook foreign investors in terms of market share.

According to Lata Pillai, Senior Managing Director and Head of Capital Markets at JLL India, this change reflects a deeper transformation rather than a cyclical trend.“The two-fold rise in core asset acquisitions shows investors are not just betting on India's story—they are building long-term wealth. Domestic capital leading the market for the first time since 2014 signals a structural transformation, not a cyclical trend.”

Two major factors contributed to this shift. REITs and InvITs deployed around $2.5 billion, accounting for 56 per cent of core asset acquisitions, while domestic private equity funds contributed nearly 30 per cent of domestic investments.

Although the foreign investors’ share proportion went down, their absolute investments actually increased by 18% per year, year. Among the sources of foreign investments, the capital from the Americas contributed the most to the momentum the city experienced. This specific source of foreign investment actually went from $1.6 billion in 2024 to $2.6 billion in 2025, an absolute annual growth of 63%.

The equity investment category continues to register significant growth and

Equity investment still remained the preferred vehicle of choice in the inflow of institutional capital, accounting for 83 per cent of the total investment in the real estate market in the year 2025. The principal reason for this is the confidence implanted in the quality of the assets, transparency of the regulatory regime, and the return prospects of the real estate sectors of India.

Investors generally shifted their preference for ownership, led strategies to debt, especially in stabilised assets and scalable platforms that provide predictable income streams and capital appreciation.

Office Sector Reclaims Top Position

After the residential assets had been the most attractive investment vehicle in 2024, the office sector returned to the top of the list in 2025, raking in close to $6 billion, or 58 per cent of total institutional inflows. Office investments were more than twice as high as the previous year, being the most significant contributors to that were strong leasing demand, the Global Capability Centre (GCC) expansion, and renewed corporate hiring.

Almost 65 per cent of office investments went to solid, income, generating core assets, which is a strong indication of the institutional preference for safer, annuity, style returns.

Dr Samantak Das, Chief Economist and Head of Research and REIS at JLL India, said the resurgence of offices reflects growing confidence in India’s commercial real estate ecosystem. “Office properties have reclaimed their position as the institutional capital magnet, attracting $6 billion through strategic investments that more than doubled from the previous year. Two-thirds of these investments were concentrated in prime core office assets.”

Alongside offices, emerging asset classes such as data centres, student housing, life sciences and healthcare real estate gained traction, highlighting investors’ appetite for diversification and future-ready segments.

Bengaluru Leads in Investments

In the geographic segment, Bengaluru was the top destination, with a share of 29 per cent in the total institutional investments in the year 2025. This was due to the presence of a thriving tech market, office space absorption, and quality assets in the city.

Mumbai Metropolitan Region (MMR) remained attractive to a large amount of capital due to its prime commercial property assets and corporate HQs. Tier-II cities lured approximately $175 million, which is around 2 percent of total, symbolizing early nascent interest in places other than top cities.

The data from the 2025 investments indicates that the Indian real estate capital market is maturing and includes an increasingly local face, equity-focused approach, and a rising trend in alternative investments. It seems that the industry indicator shows that the industry is moving to a stable phase since there are large platform transactions and a strong revival in the offices market. With sustained growth in the economy and continued development of capital markets in India, it is likely that the real estate industry will remain one of the attractive destinations not only in India but foreign institutions as well.

.png)